Analysis

of EDS' Third Quarter Financial Results

A Solid Quarter

Asia/Pacific,

Europe Lead in New Contract Sales

PHOENIX - Electronic Data Systems (EDS) reported the net

earnings of $195 million after the market closed today, down 15% from the year before, on

a 17% gain in third quarter revenues. As expected, EDS' GM revenue declined about 2%,

while its "base" business, the revenue the company derives from its other

commercial customers, surged by 24%.

For the nine months of 1998, EDS reported "base" revenues of $9.4 billion, up

21% from 1997, while the GM revenue contracted 5%, to $3.1 billion. The nine-month net

profit was up 34% from the year before to $601 million, or $1.22 per share.

After a number of special one-time circumstances are taken into account - some

boosting, others diminishing EDS' financial results - the company's overall third quarter

performance deserves a "solid" mark.

EDS's new contract sales, which set all time records in the first half of 1998, slowed

down in the third period to $2.8 billion. This puts the company on track for about a $13

billion to $14 billion total in 1998 new business volumes. If so, this would mean a

decline from the record 1997 new contract sales of $16.3 billion.

But the EDS executives were quick to point out that what they may be missing in

quantity in 1998, they are making up in quality of the new deals. "The margins on

this year's new sales are better," said Myrna Vance, director of

investor relations, answering a question during the analyst teleconference. She also added

that the current "pipeline" (of potential wins) consists of 75% of deals under

the $500-million level, versus 49% in the same period in 1997. The implication being that

the smaller deals are more profitable.

EDS's worldwide new business sales were evenly split between the U.S. and international

markets. Europe, however, continues to be a standout, increasing its share of the new

business wins from 27% in 1997, to 45% this year.

Competitive Positioning

Furthermore, in head-to-head competition with major rivals in the IT services field

(IBM, CSC, Andersen Consulting, Cap Gemini, MCI Systemhouse, Price Waterhouse and Unisys),

EDS won more than 50% of all deals in which it has competed during the quarter, said Gary

Fernandes, the company's vice chairman.

More specifically, in direct competition with the No. 1 company in the IT services

business, IBM Global Services, EDS won $750 million-worth of new contracts during the

latest period, while losing $650 million-worth to the Big Blue.

Yet IBM won $10 billion of new business in the third quarter versus EDS' $2.8 billion.

How's that possible? Does that mean that the majority of IBM's new wins were uncontested

deals?

Fernandes agreed, pointing to the Cable & Wireless (C&W - the owner of the No.

1 cable company, and the No. 2 telecom in the U.K.) deal as a case in point. Even this

"megadeal" was single-sourced, meaning not open for competition to anyone except

IBM.

How Solid Is IBM-C&W "Megadeal?"

Speaking of which, the IBM-C&W "megadeal" was a

10-year, $3 billion contract, heralded by IBM and the media in early September as

"the biggest IT services contract outside the U.S." Under the agreement, IBM was

to maintain the computer network and the billing system for C&W. But there was more to

the deal than meets the eye, according to some of the IT industry executives with whom we

discussed the situation during our September trip to Europe.

The deal "was supposed to be a two-way swap," explained one senior European

executive. "IBM gets C&W's IT business; C&W gets IBM's Global Network."

That's why the deal was single-sourced by C&W. But that's not what happened.

So when the news broke that IBM was putting its global network up for sale, and had

reportedly retained Merrill Lynch to assist it with it, "the C&W executives were

royally pissed at IBM," in the words of our European source.

So stand by for a possible unraveling of this IBM "megadeal?" Or not. Either

way, its $3 billion was, of course, included in IBM's $10 billion new business total for

the third quarter.

EDS Business Segments

Meanwhile, back to EDS' third quarter business, the Asia/Pacific region, meaning the

"P"-part of it, meaning the Australian part of the "P," meaning the

Commonwealth Bank "megadeal," showed the fastest revenue growth - up 52% over

last.

Europe chimed in with a similarly impressive 42% surge in revenues. In 1997, Europe

accounted for about $3.7 billion of EDS' revenue, or about a quarter of the company's

global business. Within that total, the U.K. represents about 35% of Europe, and the U.K.

government represents about 35% of EDS U.K. The Americas region, excluding the U.S.,

reported a 30% revenue growth in the third quarter.

Finally, the U.S., the company's biggest geographic segment (about two-thirds of the

total), which includes much of the declining GM business, chimed in with "only"

a 13% revenue increase.

Among the vertical industry segments, the third quarter revenues of EDS' financial unit

soared by 39%, followed by a 32% rise in its communications business, and a 23% increase

in manufacturing (sans GM).

Fluff Continuing to Win...

While the EDS stock has inched up to the $40-range in recent

weeks, the stockmarket is clearly still undervaluing this IT services company, at least

relative to its major rival - IBM. In a battle of fluff versus substance, fluff is

continuing to win so far.

Since August of 1996, for example, when both EDS and IBM stock were trading in the

$60-range, IBM shares have risen 140%, while EDS' have declined 35%.

Meanwhile, the two companies' business fundamentals paint a totally different picture.

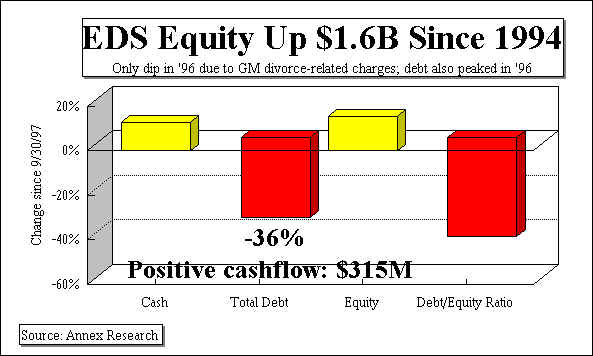

Compared to the third quarter of 1997, for example, EDS' cash is up 13%; its equity is up

15%; its debt is down 36%; its debt-to-equity ratio is down 44%; its cashflow is positive

($315 million).

In other words, it's great news for EDS' general shareholders, but bad news for bankers

and other institutional debt holders.

Now, contrast that with IBM's business fundamentals during the same period. IBM's cash

is down 22%; its debt is up 9%; its equity is down 6%; its debt-to-equity ratio is up 16%.

And IBM's cashflow was negative ($1.7 billion).

In other words, it's bad news for the general shareholders, great news for IBM bankers

and other institutional debt holders.

One key difference between the two companies, of course, has been that IBM has been

buying back its stock big time ($23 billion and counting), while EDS has not. In fact,

during today's teleconference with analysts EDS' vice chairman emphatically stated that

his company has no intention of doing it, either, at the present time.

In other words, while EDS has been investing in its business, IBM has been investing in

Wall Street's favorable stock recommendations. How else could one explain Wall Street's

failing to notice that EDS' equity has grown $1.6 billion, or 37% since the end of 1994,

while IBM's has declined $4.8 billion, or 20% during the same time frame (which happens to

be the period during which IBM has been buying back its stock). And that's in addition

to all those other fundamental business indicators which favor EDS over IBM.

IBM: The "Fluff Champ?"

In fact, IBM's "fluff ratio" (market capitalization over equity), which

currently stands at a record 7.4, is more than double that of EDS' (3.4 - DOWN [!] from

4.4 in 1994).

Based on the current market prices, IBM's market cap is about $139 billion, of which

more than $120 billion is stockmarket "fluff," and the rest equity.

In EDS' case, its market cap is about $20 billion, of which about $6 billion is equity.

Which makes the Big Blue a clear winner in the battle of the "fluff ratios."

And which sets it up as a leading candidate for the title of "fluff champion" of

the computer industry.

Happy bargain hunting!

Bob Djurdjevic

Other Charts

- EDS 1997 Intl. Revenue Shares

- EDS Quarterly New Contract Shares 1991-1998

- EDS Quarterly New Contract Values 1991-1998

- EDS Business Trends 1990-1998

- EDS Gross Margins 1990-1998

Tables

- EDS Financial Results - P&L 9M96-9M98

Also, check out "Andersen: Another

Super Year" Annex Bulletin; or "EDS

Sets New Records".

Annex Research is a well respected consulting firm serving the information needs

of today's senior IT executives, for over 28 years. For more information please call

602/824-8111.

|