|Annex

Research | Annex Bulletins | Quotes | Workshop | Feedback | Clips | Activism | Columns

![]()

The copyright-protected information contained in the ANNEX BULLETINS is a

component of the Comprehensive Market Service (CMS). It is intended for the exclusive use

by those who have contracted for the entire CMS service.

IBM FINANCIAL

Analysis

of IBM Fourth Quarter 2001 Business Results

Big

Blue Stock

to Take a Dive?

Gerstner’s Worst Fourth Quarter; Sharp

Drop in Revenue, Profit

PHOENIX, Jan. 17 - Hold on to your seats folks, and fasten your seat belts. The Big Blue stock is about to take a dive. A fairly steep dive, we figure…

No surprises there. What goes up, must come down. Especially if it rose on hot air (inflated expectations). As this writer said in a Jan. 10 Dallas Morning News article:

“The

recent (stock) upturn has been fueled, in part, by the absence of the bad

news that seemed to come every day last year.

When most companies start reporting their most recent quarterly

earnings in a few weeks, the tide could turn.

Emotions always run ahead of reason.

When the facts are in, that tends to dampen some of the

enthusiasm.”

Well, IBM’s fourth quarter facts are now in. And they are sure to dampen investors’ enthusiasm when Wall Street opens for business tomorrow morning. In fact, the last three months of 2001 represent arguably the worst fourth quarter ever reported during Lou Gerstner’s tenure as chairman (his first full year at the helm was 1994). Consider the following 4Q01 highlights:

· Overall revenues were down 11%;

· Net income was down 13%;

· Americas region’s revenue (led by the U.S.) was down 9%;

· Asia/Pacific was down 10%;

· Europe (EMEA) was down 6%;

· OEM was down 34%

· Global Services (IGS), IBM’s only “knight in shining armor,” was also down 1% - its first decline ever!

· Hardware was down 24%;

· Global financing was down 5%;

· Enterprise investments were down 20%;

· PC revenue was down 32%, plus the unit lost money ($17M pretax);

· Technology revenue was down 32%, plus the unit lost money ($293M pretax);

· Software was the only IBM business segment to have shown some growth, however modest (up 6%);

Now picture yourself as the IBM CFO having to deliver this truckload of bad news to the marketplace. You’d probably feel like Al Gore on September 11 - grateful to have lost the Florida chad contest. J

Well, with not much to rejoice about, the IBM CFO, John Joyce, bravely drove the Big Blue truckload of trouble into the post-earnings analyst conference. He painted it with BS, and called the quarter a success… relative to other industry truckloads of bad news.

When Joyce pulled the same stunt two years ago, blaming the IBM woes on the Y2K that time, we called it a “Slam-Dunk of Bunk,” (Jan 19, 2000). This afternoon, Joyce has outdone himself. Make it a “Grand Slam-Dunk of Bunk!”

Yet the analysts bought

it. At least that’s the

impression one got by the meek and mild tone of their questions.

So don’t look for a huge stock slide tomorrow, even though a free

fall is what Armonk richly deserves.

At least based on the above facts (also see the chart and our special Appendix

- On Wall Street, Big Blue Sky Always Bluer - Next

Year! (1987)

A part of the reason for Wall Street’s permissiveness of poor business performances is that there is about three trillion dollars being “parked” by investors in short-term market instruments currently, according to our sources in the banking community. All this money is seeking a sinkhole into which to drop. Just like 15 years ago (see the Appendix).

Of course, Wall Street won’t put it that way. They will call it an opportunity. The Big Blue is just one of many sinkholes… oops, opportunities. And it is a big one at that, as you saw from the above highlights.

Segment Analysis

Geographies. One good business these days is war business, seems to be the message that emanates, both from IBM’s fourth quarter results, and from the IBM CFO comments.

“Public sector was strong across all geographies,” Joyce said. But the demand among the small and medium size company was weak, he added. He blamed the softness of the PC market on the latter.

Add another coat of BS to the Big Blue truckload of trouble. For, a majority of the PCs that IBM sells goes to large corporations. In the U.S., for example, two-thirds of its fourth quarter PC revenues came from the “direct” sales channel.

In fact, had IBM diversified more and sooner toward the small and medium company markets, as we suggested back in 1996 (see “Louis XIX of Armonk,” Aug 26, 1996), the company would not be such a large sinkhole right now.

As it turned out, however, the Big Blue had the “foresight” to get out of the federal government business back in 1994 (!?), when it sold its Federal Systems Division to Loral Corp. (see Annex Bulletin 94-06, Jan 25, 1994). Which meant that IBM dug itself even deeper into a hole. Of course, it thought it was cashing a post-Cold War “peace dividend.”

Meanwhile, back to the fourth quarter, IBM revenues in the Americas region, which encompasses the U.S., Canada and Latin America, and accounts for about 44% of the worldwide total, slipped under $10 billion (to $9.8 billion), a 9% decline from a year ago (down 8% in constant currency).

IBM’s business in Europe, Middle East and Africa, the second largest segment at 28% of global revenues, fared somewhat better. But it also dropped by 6%, both as reported and in constant currency.

Asia/Pacific declined by 10% (down 1% in constant currency), while the OEM sector plummeted by 34% (down 33% in constant currency).

Overall, IBM’s fourth quarter revenues ($22.8 billion) were down 11% from the year before totals (see the chart). Which puts them about one billion dollars short of Wall Street’s expectations.

Services. Perhaps the biggest disappointment in IBM’s fourth quarter results was that its “knight in shining armor;” its “one string violin” in the 1990s; its only remaining “crown jewel” - IBM Global Services - is no longer any of the above. For the first time ever (!), the IBM services revenue actually declined (down 1%) from a year ago.

When first signs of trouble started to show up in the IGS results two years ago, the Big Blue tried to sweep them under the rug by a sweeping statement. It was due to customers’ reticence to spend money because of the Y2K bug, we were told. But it will all get better from there on.

Back then, we said in a subheading to our “Slam-Dunk of Bunk,” Jan 19, 2000) report: “Biggest Surprise: A Sharp Drop in Services Revenue Growth - Up Only 2%!”

“A

precipitous drop (down to only 2% in 4Q99) in the growth of IBM Global

Services revenues, IBM’s “crown jewel” and the only working string

in its violin, should give us cause for optimism.

Why? Because “we’re pleased

the Y2K issue is behind us,” according to Joyce.”

Well, what was considered bad news (“a precipitous drop in growth”) two years ago, is now even worse bad news - a plain vanilla decline in revenues.

This time, Joyce blamed it on the late timing of some fourth quarter contract signings. As a result, he said, IBM could not book as much revenue as it expected in the fourth quarter.

Of all the buckets that he IBM CFO used up painting coats of BS over Armonk’s truckload of trouble, this was probably the biggest.

Everybody knows that service contracts are annuities; that revenues are usually earned over a five to 10 year-contract period. Everybody also knows that it usually takes six to nine months for a mega-contract to start to produce revenues and profits for a vendor. So the fourth quarter contract signings ($15 billion, according to IBM) could not have been reasonably expected to contribute much to the company’s top and bottom lines until well into 2002.

Unless, of course, the Big Blue is into something it is not supposed to be in - such as “aggressive accounting” - booking revenue and earnings early (for more on that, check out the “Enronizing IBM?” part of this report).

Meanwhile, IBM’s backlog of $102 billion was only up $5 billion over that at the end of the third quarter, despite $15 billion in new business the company is supposed to have added to it in the fourth period.

Which suggests that IBM’s sinkhole is also getting deeper because of the customer contract cancellations/expirations are continuing to run at a high rate. In fact, they appear to be accelerating.

In the last two years, IBM’s cancellations/expirations averaged about $8 billion per quarter. But in the fourth quarter of 2001, they shot up to $10 billion (see the chart).

Plus

there is a possibility of “aggressive accounting” in this area, too.

One IBM insider told us in late November that the company had

changed the definition of its “backlog,” but has failed to communicate

that to the outside world:

“Traditionally

we think of the definition of backlog as orders taken, goods sold,

services booked, a done deal. Now IBM is using as a reference market

opportunity, market segment, ability to sell to NOT BOOKED, NOT SOLD.”

In other words, IBM seems to be substituting what the rest of the IT services industry calls a “pipeline” (of opportunities) for “backlog” (firm orders taken), according to this insider.

Which implies that Wall Street’s and other outsiders’ perception of IBM services’ success may be considerably greater than reality. IBM’s declining revenues in the face of record sales hint in that direction.

Servers. IBM’s fourth quarter hardware sales were dismal, declining a whopping 24% since a year ago quarter. Making matters worse for the bottom line, the hardware gross profit dropped even more steeply. This resulted in a gross margin of only 26%, down from 30% in the fourth quarter 2000 - less than even the IT services margins! (28%, including maintenance).

Given that hardware still represents a very large (39%) share of IBM’s business, trouble in this sector tends to wreak havoc throughout the Big Blue financial statements. As a result, IBM’s Joyce had to dig deep and long through his truckload of trouble to find something good to say about the IBM hardware lines of business. And he found it in perhaps a most surprising area.

It was IBM mainframes (now dubbed zSeries) that were the bright light of the fourth quarter. For the first time since 1989, revenues went up, Joyce rejoiced.

But the official IBM statement said they were “essentially flat,” thus contradicting the CFO’s exuberance during the analyst teleconference. This roughly squares with a meager (+12%) MIPS shipments increase that IBM also reported for the fourth quarter.

Furthermore, the official IBM financial statements show that the Enterprise Systems revenues, which include mainframe and storage, were down 13% in the quarter. And that their related pretax profit dropped even more precipitously (down 18%) during the same period.

So did Joyce misspeak? Not exactly. He did say that the 15% zSeries revenue increase was for the full year. But he spoke about that in the context of the fourth quarter, and while showing the slide reflecting the fourth quarter results.

So guess one could call this “Big Blue BS with a twist.” For, after all the hoopla, hat-tossing and cheering about the supposed IBM mainframe growth, the cold fact remained that the fourth quarter of 2001 marked the period when a temporary resurgence of mainframe demand - STOPPED!

Yet, no analyst challenged Joyce on his joyous mainframe proclamations during the question period.

But one person did flatter the IBM CFO with a leading question. Did he expect IBM to have gained share in the Unix market? Joyce replied in the affirmative. He said that since other Unix vendors are having so much trouble that their revenues are declining 40% or more, IBM’s Unix drop of “only” 20% will mean just that - a market share gain! J

See how deep IBM spokesmen have to reach to scrape the bottom of the Big Blue barrel these days to come up with a positive spin on negative financial news? J

Furthermore, Joyce said that IBM was also doing great at the top of its Unix product line, but for the late start of the “Regatta” server shipments (Dec. 14).

Oh, shucks… Poor Big Blue… being hit from all sides with all this “bad luck!” First, it’s the economy (stupid!); then services customers don’t want to sign until the year end; then Unix buyers want to buy the IBM servers, but IBM is all out. Sorry.

And who, do you suppose, makes the planning decisions about when the IBM products are to be ready to ship? Certainly not the customers, right?

So before we bring out the violins to serenade IBM’s bad luck, let us point out who is benefiting from IBM’s Unix marketing. Yes, your guessed it… the Big Blue archrivals, such as Sun Microsystems, for example. They are filling the demand that IBM has generated but cannot meet.

While some analysts questioned whether competitors (IBM) were seeing stronger growth than Sun, Ed Zander, Sun’s chief operating officer, highlighted the company's strength in the high-end server market.

“I think if you take the server business and what we're doing in the high end, we lead everybody in that class,” he said. “We're very pleased, especially with all the money IBM is pouring into advertising” (see the New York Times, Jan. 18).

So yes, there are good reasons for one to feel sorry for IBM. But bad luck isn’t one of them. Pathetic marketing - ironically by a company once regarded as the best of breed in that respect - seems like a better one.

Technology and PCs. The IBM CFO breezed through the company’s two most troubled areas like a bullet train through a whistle stop. He finished his “review” of the PC and Technology sectors in record time. And no wonder. Both sectors’ revenues were down 32% in the fourth quarter. Both lost money… PCs lost $17 million pretax, while Technology dropped $293 million of red ink to the same line.

We’ve said many times in the past that IBM should have gotten out of both of those businesses (see “IBM Break-up,” Jan. 1996). But this would have diminished “Louis XIX’s” Big Blue empire by some $24 billion or more in revenues.

So proving that he is an amateur empire-builder rather than a savvy entrepreneur, Gerstner has now ended up with a dwindling empire anyway. No pain for the IBM chairman personally, though. He will ride off into the Florida retirement sunset with tens of millions of dollars gained from insider sales of his IBM shares and options (see “Greed Breeds Incest,” Nov. 1998).

Now, if the preceding reminds you of the $1.1 billion in insider sales from which Enron executives benefited before the October collapse of that erstwhile Wall Street darling and highflier, you won’t be alone.

Pravin

Banker, a financial advisor at small investment bank the Financial

Network, says the accounting profession, stung badly by Lucent, Enron and

other imploding corporations, “will want to peel the onion and look

under the covers,” according to a Jan.

17 CBS Market Watch.com report.

Greater accounting vigilance will lead to questions at Dow-traded

companies, including computer giant IBM, says Banker, who is based in

Connecticut.

Here’s

an excerpt from that CBS report:

“To be sure, skeptics have long questioned the accounting practices of IBM and other technology companies. Banker says accountants will run a fine-toothed comb over companies that:

"IBM

will crack, and so will Microsoft," says Banker. "The gun-shy

accountants will make sure of that."

Last

year was a record one for bankruptcies: 255 stock-market companies filed

for Chapter 11 compared with 176 in 2000, a 45 percent increase.”

Of course, you’ve been hearing us point out for over five years now that “financial engineering” has been the only new line of business the Gerstner administration has ushered into Armonk. We are no longer the lone voice in the wilderness. In June 2000, the Fortune magazine also picked up that chant (see “Fortune on IBM,” June 2000). And now, “aggressive accounting” knives are getting unsheathed all across the media and financial institutions.

Finally, the governments are also getting into the act. Securities and Exchange Commission (SEC), whose lax enforcement of accounting and other trading rules helped make the Enron-size failures possible, is waking up to the fact that it is supposed to protect the investor, not the company whose shares are being traded.

Responding to a growing criticism of accounting practices stemming from the collapse of the Enron Corporation, Harvey Pitt, a former Wall Street lawyer and the new head of the SEC, proposed today (Jan. 17) that the accounting industry should be policed by a group dominated by outside experts instead of policing itself.

But Pitt did that only after coming under fire himself for his close ties to Wall Street. And from the Wall Street Journal at that, of all media outlets! (see “Pitt Peeves,” WSJ, Jan. 17).

Furthermore, speaking in Connecticut the same day, the state attorney general asked the state's accountancy board today to consider whether to revoke the licenses that let Arthur Andersen, Enron's auditor, work for corporations in that state.

And last but not least, the Enron board fired today its beleaguered auditor, Arthur Andersen, amid finger-pointing between two former cohorts in financial scams.

Don’t you love it how “everybody” turns pristine and lily white when governmental, legal and financial snoops start to poke at a corporate carcass, especially one as large as Enron’s? Next to practicing greed in good times, kicking someone when he is down seems to be a favorite boardroom sport.

The same goes for the media. Suddenly, everyone is the wiser, even those who once lauded Enron’s financial savvy, and who admired its chairman Ken Lay’s Washington and Wall Street power.

“How Wall Street Greased Enron's Money Machine,” (WSJ, Jan. 14), and “A Bubble No One Wanted to Pop” (NYT, Jan. 14) are two among many stories, one from the Journal, the other from the Times, that exemplify the newfound “slash and burn” style of reporting about Enron’s woes.

The Times’s piece is particularly significant, and not just because it was published on the front page of the New York daily. To appreciate why, check out the following, slightly edited, excerpt from it:

IBM Wasn’t as Mighty as Highflying

Stock Made It Appear

By GRETCHEN MORGENSON

(That) the world is now awakening to is that the IBM Corporation (news/quote) was not much of a company, but its executives made sure that it was one hell of a stock.

In recent years, IBM came to exemplify the productivity miracle that new technologies were thought to have bestowed on astute companies across America. With the odor of scandal all around it, IBM, once an innovative computer company, has instead become an indictment of the anything-goes approach to business that characterized the late 1990's. The bull market euphoria convinced analysts, investors, accountants and even regulators that as long as stock prices stayed high, there was no need to question company practices.

"IBM is the prime example of all the

things that were allowed to go wrong during the stock market mania,"

said William Fleckenstein, president of Fleckenstein Capital, a money

management firm in Seattle. "This wall got built brick by brick in

broad daylight in the 1990's by companies doing whatever they had to do to

make their numbers, being willing to sacrifice the long-term well-being of

the company so that the executives could get rich."

Sound familiar? If unsure, check out “IBM Smoke and Mirrors Game: Mortgaging Its Future?” (Apr. 1997).

And the IBM insiders became rich indeed.

Thanks largely to munificent stock option grants, which they turned into

shares, they sold hundreds of million dollars’ worth of stock from 1996

to mid-2001.

Sound familiar? If unsure, check out see “Greed Breeds Incest,” (Nov. 1998).

Mostly on the strength of the stock

buybacks and the highflying shares, IBM executives were able to convince

investors, bankers, analysts, accountants, debt-rating agencies and even

IBM's own employees that its promise was real, its financial results

genuine and its growth never-ending.

Sound familiar? If unsure, check out “Is Big Blue Back?” (Forbes column, June 1997).

Now the spotlight in the IBM follies is trained on the nation's capital. But the story of the company's rise and fall, and the retirement savings its workers lost, inevitably leads back to Wall Street.

IBM's executives were surely smart enough

to know that once they had convinced bankers, brokers and accountants of

the company's strength, all parties could pretty much be counted on to

keep the myth of solidity alive, even after problems arose. When questions

were first raised about partnerships that should have been listed in

financial statements, true believers could be relied on to drown out

naysayers.

Naturally, given the millions of dollars Wall Street firms generated selling IBM's shares and bonds to investors, analysts were among the most vociferous defenders of the company, even after its stock began to fall.

Of course, if a company wants to mislead

its investors, analysts and accountants, there is probably little that can

be done to stop it. IBM's auditor has said that it was misled.

Because IBM operated in a largely unregulated arena, the company

recorded revenue and profits that made the economic status of its business

appear larger than it really was.

And so on, and so forth…

Summary

By now, we are sure you’ve figured it out. The preceding is a fictitious New York Times story based on a real one about Enron. Our “slight editing” mostly consisted of substituting IBM for Enron, and computer or IT services industry terms for those used in the energy sector.

Could something like this ever happen to IBM? Well, a Chapter 11 bankruptcy filing isn’t likely any time soon. Despite its recent woes and some questionable financial and business practices, IBM still nets $7 to $8 billion a year at the bottom line. Even if hot air due to “aggressive accounting” is taken out, chances are there will still be plenty left over at the bottom line for the shareholders.

But a story like the above fictitious one could be written one day not only about IBM, but also about other corporate giants. At least those who have fallen for the allure of Wall Street-pleasing “financial engineering,” or quick buck “aggressive accounting,” instead of making their money the old-fashioned way - by outselling and outsmarting their competition on Main Street.

So a good rule of thumb is this… if a company whose shares you own panders to Wall Street, and engages in “financial engineering” - dump it! Even if it hurts right now. Sooner or later, you’ll be glad you did.

Happy bargain hunting!

Bob

Djurdjevic

P.S. In early morning trading on Jan. 18, IBM fell $6.42 to $113.48 while Microsoft tumbled $3.16 to $66.70. The selling spread to other technology issues, including Intel, whose shares fell 93 cents to $33.60.

|

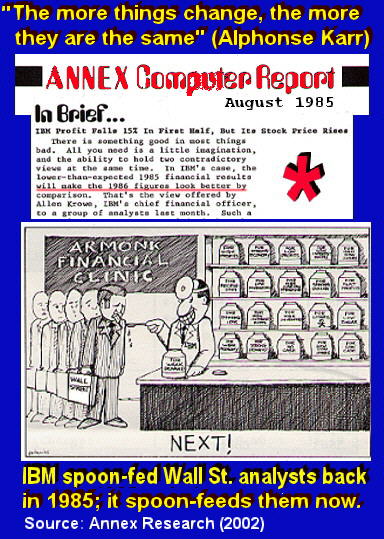

On

Wall Street, Big Blue Sky Always Bluer - Next Year! (2002) "The

more things change, the more they are the same" (French

philosopher Alphonse Karr, 1809-1890). |

||||||

|

|

|

|

|

|

|

|

|

|

Annex

vs. Wall Street IBM Forecasts 2001/2002 |

|

||||

|

|

|

as

of June 2001 |

|

|

|

|

|

|

2001 |

|

2002 |

|

|

|

|

|

EPS |

Revenue |

EPS |

Revenue |

|

|

|

|

|

|

|

|

|

|

|

Annex |

$4.19 |

$92,600 |

$4.31 |

$95,600 |

|

|

|

Wall

Street |

$4.84 |

$92,700 |

$5.48 |

$99,200 |

|

|

|

|

|

|

|

|

|

|

|

Actual |

$4.35 |

$85,866 |

|

|

|

|

|

|

Annex

vs. Wall Street IBM Forecasts 2002 |

|

|

|||

|

Annex |

|

|

$3.73 |

$85,100 |

|

|

|

Wall

Street |

|

|

$4.81 |

$91,300 |

|

|

|

|

|

|

|

|

|

|

|

Wall

St-Annex Diff (Jan02) |

$1.08 |

$6,200 |

|

|

||

|

Wall

St-Wall St Diff (Jan02-Jun01) |

($0.67) |

($7,900) |

|

|

||

|

On

Wall Street, Big Blue Sky Always Bluer - Next Year! (1987) "The

more things change, the more they are the same" (French

philosopher Alphonse Karr, 1809-1890). ------------ Volume

IV, No. 87-37

July 14, 1987 (c)

Copyright 1987 by Annex Research.

All rights reserved. WHY "IBM/INDUSTRY WATCHING" IS NOT A TEAM SPORT PHOENIX,

July 14, 1987 - Several years ago, I had the privilege of working

at Judge Edelstein's chambers for a few days (former Chief Judge

of New York's Second Circuit, who also presided over the 13-year

antitrust battle between the Justice Department and IBM).

On one occasion, a messenger delivered a package from a

large Wall Street law firm. Unfortunately,

the materials in the package were late.

"How many lawyers do they have, Jonathan?" the

Judge asked his law clerk, referring to this respected Wall Street

firm. "I think

about 240, at the latest count," Jonathan replied.

"Too bad they don't hire one good one," the Judge

snapped, as he dispatched the courier out the door in a hurry. On

another occasion a few months ago in Sydney, Australia, Dr. Gene

Amdahl, told me that designing systems was a job for only one or

two people. One

sometimes needs "a cast of thousands" to do the coding,

but only one person setting the direction.

Otherwise, all those people may end up pulling together

splendidly, but alas, the wrong way.

Dr. Amdahl said that he thought that IBM watching was also

the kind of work where "one good one" can pull more

weight than many others. What

happened today on Wall Street illustrated once again why, like

being a good lawyer or a systems architect, the IBM/industry

watching is not a team sport.

IBM's second quarter earnings were down 10%, just as many

Wall Street analysts had boosted their earnings estimates.

Even though the Wall Street indeed has hundreds of people

going through the soothsaying motions, every once in awhile it

ends up at the short end of the stick. Wall Street/Annex -- On The Opposite Sides Of Fence For

several days preceding IBM's release of its second quarter

results, the business press was buzzing with rumors of upbeat news

about IBM. The

optimism was fueled by the fact that at least six of the major

Wall Street firms' analysts either increased their estimates for

IBM, or made statements to the press which suggested that they

should (see the WALL

STREET JOURNAL-7/08/87 and the DOW JONES wire-7/13/87).

It is not surprising, therefore, that on July 13, the day

before IBM was to release its latest results, its stock jumped 2

1/4 points in anticipation of a good report card from the company.

Meanwhile,

at the same time as some of our respected Wall Street colleagues

were telling their followers to expect an upbeat IBM report today

(at about $2.15 per share, they were implying net earnings of

about $1.3 billion), our IBM Revenue/Earnings Model clients were

being told of our LOWERING of the second quarter IBM earnings

estimates from $1.3 billion to $1.14 billion.

What were IBM's actual earnings?

$1.18 billion! Predictably,

IBM's stock plunged 2 3/8 points today, despite a 28.38-point

surge in the Dow Jones Industrials Index. By

the way, we weren't alone in suggesting a cautious stance

vis-a-vis IBM. It was

refreshing to see a relatively young analyst, Stephen Milunovich,

of First Boston, sticking to his guns, i.e. his earlier estimate

of $1.90 per share for the second quarter.

As it turned out, he was right while Merrill Lynch, E.F.

Hutton, Drexel Burnham, Gartner Group, Thomson McKinnon, Weil

& Associates -- the six firms quoted by THE WALL STREET

JOURNAL and the DOW JONES wire - were wrong, and by a considerable

margin, too. Lower Prices In 1987, Lower-than-expected 3090 Volumes Evidently,

some of our Wall Street colleagues paid more attention to the

local gossip than to the FACTS which determine IBM's and other

vendors' destinies. For, were they paying attention to the latter, some might

have realized that the factors to which IBM's Akers attributed his

own optimism -- the earlier than expected shipments of the PS/2,

the 9370, and the 3090-600E -- would only have a minimal impact on

the company's 1987 net earnings.

That's because in the case of the first two product lines, we are dealing with relatively low margins (see CMS BULLETIN 87-36, 7/06/87). As for the 3090-600E, this CPU's contribution to 1987 profits is likely to be offset by the lower shipment volumes of the 3090-300E and 400E, as well as the aggressive price cuts exacted by the PCMs. In other words, we said that IBM will surpass its 1986 shipment and revenue levels, but its profit margins would nevertheless still form a trough (see the charts and CMS BULLETIN 87-35, 6/29/87). An IBM spokesperson today essentially confirmed such a view. Commenting about the outlook for 1987, he said that IBM was very happy with the second quarter results, and that the company expects "a modest increase in shipments and revenues for the year." Notice -- he did not mention PROFIT increases. |

---

Sound familiar? (Annex Ed. - Jan. 18, 2002) J ("The more things change, the more they are the same" - French philosopher Alphonse Karr, 1809-1890).