Annex Bulletin 2008-21 October 17, 2008

A partially OPEN CLIENT edition

Recent... ![]()

Facts Fight Back Fears (IBM releases detailed third quarter results)

Fear Trumps Fact (Total disconnect between stock market and IBM business fundamentals)

IBM FINANCIAL

Updated 10/21/08, 10:00AM PDT; adds Mainframe, System p charts, comments...

IBM's third quarter still shines amid gloom and doom on Wall Street

Facts Fight Back Fears

Detailed results confirm preliminary optimism

|

"Where ignorance is bliss, 'tis folly to be wise" (Thomas Gray, 1716-1771) |

SCOTTSDALE, Oct 19 – "In a market driven by fear, logic and reason can be dangerous to your financial health," we said in our Oct 9 report. Or, as Thomas Gray put it more than two centuries ago, "where ignorance is bliss, 'tis folly to be wise" (Thomas Gray, 1716-1771). We added that, "there is a total disconnect at the moment between the stock market and the business fundamentals."

The preceding point and the charts were first published on Oct 9, after IBM released its preliminary third quarter results ("Fear Trumps Fact", Oct 9). It was the day the Dow slumped another 679 points (see "IBM, Internet losses lead broad tech plunge at close", Dow Jones' MarketWatch, Oct 9).

"Fear won.

Reason lost. And least for today," we summed it up.

Well, October 17 was another day. When IBM released its detailed third quarter results a week later, its stock rallied (see the right chart). And the market as a whole finished the week slightly up, for the first time in weeks.

Whew. It was a welcome breather after weeks of emotional panic selling.

Business Segment Analysis

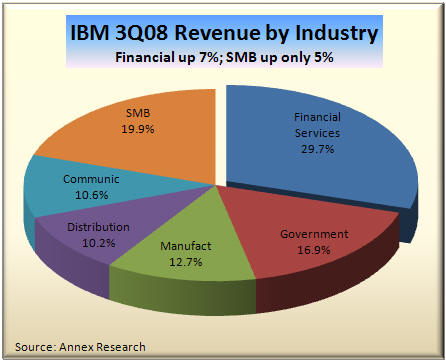

Industries.

Let's start with the industry sector analysis this time, as the myths about

IBM's alleged exposure to the Financial Services woes has led to emotional

selling of the stock in the last several months.

True

enough, this is the largest business segment.

True

enough, this is the largest business segment.

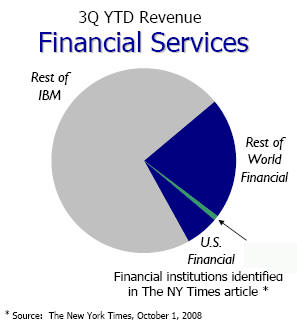

But on a global basis, this sector's revenues were up 7% as reported (up 2% in constant currency - see the chart). And over three quarters of that total comes from overseas market, rather than the sick Wall Street puppies (or giant pandas, of you prefer, given their size). So, while the IBM U.S. financial services revenues were down 1%, slightly less than in the second quarter, the overseas business was up in double digits (+10%).

Furthermore ,

60% of IBM's financial services business is annuity revenues (right chart

below). Which means that the company is relatively well cushioned from

quarterly swings in demand.

,

60% of IBM's financial services business is annuity revenues (right chart

below). Which means that the company is relatively well cushioned from

quarterly swings in demand.

In fact, the biggest disappointment for us was the fact that the SMB sector which IBM has been hailing as its key growth engine, delivered only 5% growth in the third quarter (up only 2% in constant currency). The manufacturing segment revenues actually declined in constant currency (up 2% as reported) - the worst sector performance of the six that IBM reports every quarter.

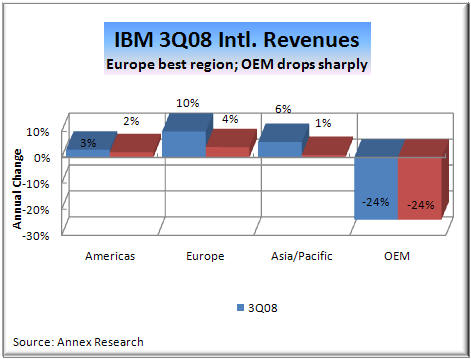

Geographies. By contrast to a quarter a year ago, Europe - a traditionally slow market during the summer vacation months - turned in the best geographic performance in the last three months. It was up 10% as reported (up 4% in constant currency). The Americas also managed to grow despite the alleged economic woes, up 3% (up 2% in constant currency.

Interestingly, IBM's normally fastest growing geographic

segment - Asia/Pacific - was the lagga rd

this time, managing to eke out only a 1% growth in constant currency (up 6%

as reported). That's mostly because of disappointing results in Japan

and China, the latter ostensibly because of the Beijing Olympics, which

distracted the buyers, according to IBM.

rd

this time, managing to eke out only a 1% growth in constant currency (up 6%

as reported). That's mostly because of disappointing results in Japan

and China, the latter ostensibly because of the Beijing Olympics, which

distracted the buyers, according to IBM.

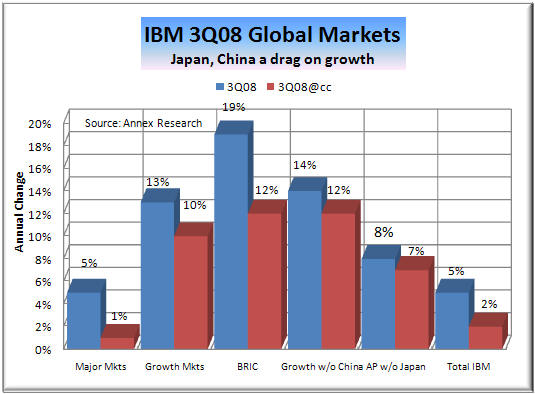

The chart on the right provides additional granularity for IBM's global markets. With exception of China, generally the growth has come from emerging markets which grew in double digits (up 14% as reported, and up 12% in constant currency). China grew by 3% as reported but was down 4% in constant currency. The other three BRIC countries - Brazil, Russia and India - all grew in double digits, pushing the group total to 19% growth as reported, and 12% in constant currency.

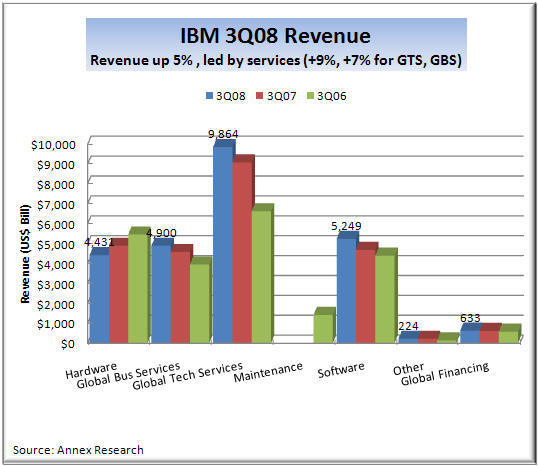

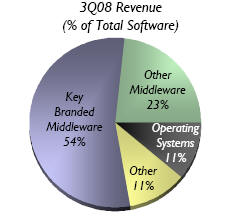

Software. Software was

again a standout among IBM's horizontal business segments. its revenu e

was up 12% as reported and 8% in constant currency. Within that total,

the branded middleware (left chart) grew by 15%, with Information

Management, Rational and Lotus brands leading the way with 26%, 23% and 10%

growth respectively.

e

was up 12% as reported and 8% in constant currency. Within that total,

the branded middleware (left chart) grew by 15%, with Information

Management, Rational and Lotus brands leading the way with 26%, 23% and 10%

growth respectively.

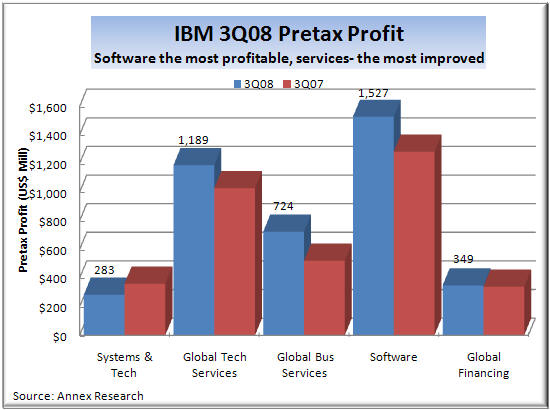

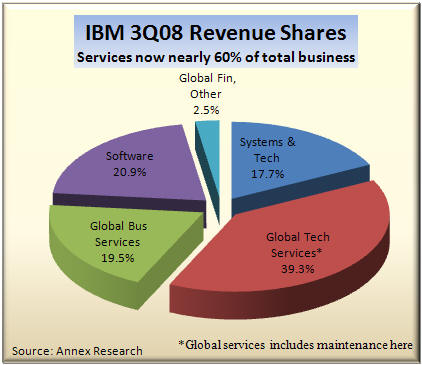

But software's most important contribution to IBM is to its bottom line. With gross margins of 85% and pretax margins of 26%, software is by far IBM's most profitable segment (right chart). The software segment pre-tax income grew 19% since a year ago to $1.5 billion, even after all the acquisition-related expenses.

Services. IBM's two

Global Services segments - GTS and GBS - also distinguished themselves by a

strong profit margin performance. GTS' jumped from 00.6% to 32.7%,

while GBS' surged from 22.9% to 27.4%. Overall, IGS' pretax profit was

up 23% on revenue growth of 8% as reported (4% in constant currency).

This was the highest level of services pretax margins in six years, IBM's Loughridge said, adding that this was "especially important given that we did it in the seasonally challenging third quarter."

New contract signings were $12.7 billion at actual rates, down 4 percent.

The two IBM services units now account for nearly 60% of IBM's total revenues. Given the annuity nature of services, these business segments also provide a relative cushion against the sudden swings in demand.

So IBM’s services strategy is clearly paying off. In times or economic prosperity, IGS is helping customers grow faster. In times of business slowdowns, such as right now, it is helping them save money and restructure for the future. Putting it another way: If IBM were still just a hardware-driven company, its business would be down right now. Instead, it is thriving despite the generally pessimistic global climate.

Hardware.

Yet even in the hardware segment, there were bright stars. Mainfram e

has not only regained its former luster, it is shining brighter than ever.

The System z revenues were up 25% since a year ago. Given that many of the

beleaguered financial institutions are also some of the biggest mainframe

customers, the strong IBM results are also is also a pretty good indicator

that its virtualization strategy and the emphasis on “green” datacenters

that save customers money on energy and other resources, is working well

across the board.

e

has not only regained its former luster, it is shining brighter than ever.

The System z revenues were up 25% since a year ago. Given that many of the

beleaguered financial institutions are also some of the biggest mainframe

customers, the strong IBM results are also is also a pretty good indicator

that its virtualization strategy and the emphasis on “green” datacenters

that save customers money on energy and other resources, is working well

across the board.

Speaking at a System z Summit in New York on Sep 18, Anne Altman (left), who heads up the IBM mainframe program, said that "even in these challenging times, we're still seeing a lot of interest in Z10" (IBM's new top-of-the-line mainframe).

She added that IBM has been able to attract about 1,400 ISVs (Independent

Software Vendors) to the z platform, as well as 481 universities and

colleges who are now offering mainframe education to some 50,000 students

around the world.

As a result, the System z managed to attract 24 new accounts in the first half of the year (18 in the U.S.). So "the trajectory is very positive," she summed it up.

Karl Freund, the head of mainframe worldwide marketing (right), said at the same New York Summit that, "the System z is at a perfect point of a 'perfect storm'." Freund, who used to be in charge of System p marketing in his prior job, said that a special accelerator based on System p will be brought into the z environment.

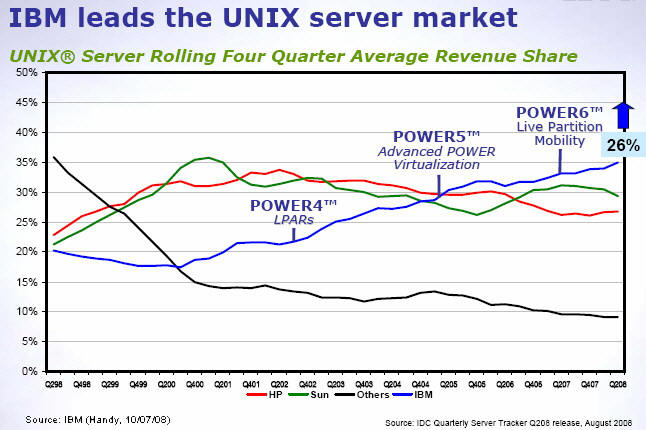

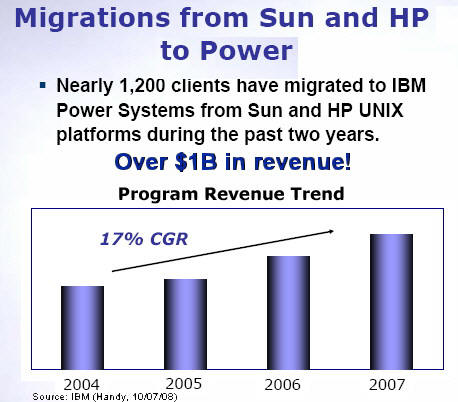

Speaking of System p, the strong

System p performance (up 7% in the third quarter) confirms the same

trend. IBM’s Unix platform, now merged at the high end with the System i,

has been the first to introduce the “green” Power 6 chips (in May of last

year). So it is also thriving by winning share from HP and Sun, even though

the Unix market as a whole is shrinking (see left above chart).

(see left above chart).

Nearly 1,200 customers have migrated from Sun and HP to IBM during the past two years, said Scott Handy, the head of System p marketing, at an Oct 7 teleconference (see right above chart). They represented over $1 billion in additional revenue.

Offsetting those bright spots are sharp declines in legacy System i and x servers (down 82% and 18% respectively) and in chip OEM technology sales (down 27%). Storage and retail (POS) products also declined but at lower rates.

Summary & Outlook

As you can see from the preceding, there is no place for gloom and doom among the IBM business results. They were not record-breaking figures, such as those that Accenture reported in late September for its fourth fiscal period ("Accenture's "Par Excellenture" Quarter", Sep 2008), but Big Blue demonstrated a resilience of its global strategy.

And the results pretty well matched up with our expectations (Annex Clients see below for detailed 3Q08 P&L figures that show actual vs. our forecast).

Software, emerging markets and services showed that companies can make money and deliver solid growth even at times when Wall Street bankers are looking for rocks to hide under. It remains to be seen if the IT leaders can continue to do so in the fourth quarter, usually the strongest period for companies with Dec 31 fiscal year ends.

|

Annex Clients: CLICK HERE for detailed IBM 3Q08 P&L tables & charts |

Happy bargain hunting!

Bob Djurdjevic

![]() Click

here for PDF (print) version

Click

here for PDF (print) version

![]()

For additional Annex Research reports, check out... Annex Bulletin Index 2008 (including all prior years' indexes)

![]()

Or just click on SEARCH and use "company or topic name" keywords.

Volume XXIII, Annex

Bulletin 2008-21 Bob Djurdjevic, Editor 8183 E Mountain Spring Rd, Scottsdale, Arizona 85255 (c) Copyright

2008 by Annex Research, Inc. All rights reserved. |

Home | Headlines | Annex Bulletins | Index 1993-2008 | Special Reports | About Founder | Search | Feedback | Clips | Activism | Client quotes | Speeches | Columns | Subscribe

Also check out...![]()

![]()

Accenture's "Par Excellenture" Quarter(Blowout 4Q lifts Accenture over EDS to #3 spot in IT services world)

Just Say No to Greed 2! (Proverbial IT babies being thrown out with Wall St bathwater)

"Beat the Street" Drumbeat Continues (Analysis of HP's 3Q08 business results)

Big Blue Stock Sags on "No News" Days (Analysis of IBM institutional shareholdings)

IBM Delivers Explosive Quarter (Big Blue firing on all cylinders - analysis of 2Q08 results)

MacAttack Falters at Foot of Mount Vista (A story about yet another attempt to break away from Windows)

Minting "Green" into Greenbacks (An update to our five-year forecast for IBM)

Better Late Than Never - Analysis of a rumored HP takeover of EDS

IBM "Places" By a Nose over Google - Analysis of Top 20 IT Cos stock and business performances

Big Blue Takes Chill Off Wall Street's Spring (Analysis of IBM's first quarter business results)

Just Say NO to Greed - Killer of Dreams! (An editorial comment about subprime financial crisis)

The z10 Lifts "Big Green" (Analysis of IBM's new mainframe announcement)

HP Beats the Street Again (Analysis of HP's 1Q08 business results)

Capgemini's Great Valentine's Day Gift (Analysis of Capgemini's 4Q07 and FY07 results)

Profit Drops, Stock Follows (Analysis of EDS's 4Q07 results)

Profit, Revenue Surge, Lifting Stock, Too (Analysis of CSC's 3Q08 results)

Services, Emerging Markets Boost IBM (Analysis of IBM's full 4Q07 results)

Big Blue Shines in 4Q (Analysis of IBM's preliminary 4Q07 results)

Microsoft Still Wall Street Darling (Analysis of institutional holdings of Top 10 IT Cos)