Annex Bulletin 2008-23 December 18, 2008

A partially OPEN CLIENT edition

Recent...

![]()

Accenture's "Par Excellenture" Quarter(Blowout 4Q lifts Accenture over EDS to #3 spot in IT services world)

Just Say No to Greed 2! (Proverbial IT babies being thrown out with Wall St bathwater)

IT SERVICES

Updated 12/18/08, 7:30PM PDT

Analysis of Accenture's First Quarter FY09 Business Results

Bright Beacon in Sea of Gloom & Doom

Company Exceeds Wall Street Expectations with Strong Quarter, But Lowers FY09 Estimates

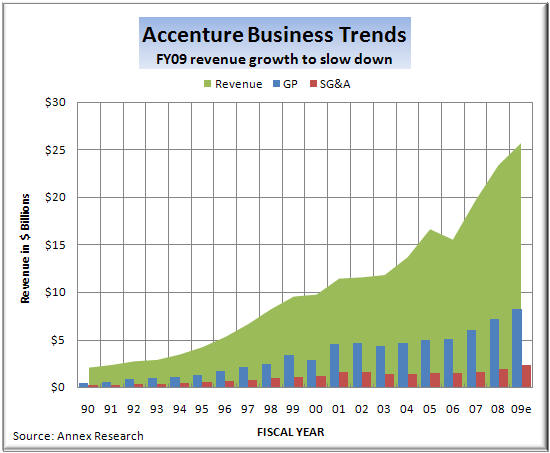

SCOTTSDALE, Dec 18 – Accenture was the first major IT company to report business results that include the disastrous calendar fourth quarter, the worst recession in the U.S. economy since the Great Depression. And what Accenture's numbers showed should calm investors' fears and embolden the company's shareholders. Net (EPS) surged by 24% to $0.74 per share on a 6% revenue growth (up 9% in local currency) to $6 billion. Operating income was up 12%, boosting the operating margin by 0.7% to 13.5%.

No signs of recession in those numbers, are there?

Yet the company lowered the outlook for the current (second fiscal) quarter

and for the full year 2009 (that ends Aug 31), citing negative foreign

exchange impact as major factor. Accenture's revised business outlook

for the full fiscal year assumes a currency translations impact of negative

8% to 10%. The company previously

assumed

a negative 2% to 4%.

assumed

a negative 2% to 4%.

That's a curious rationale, especially in light of yesterday's Fed decision to drop the interest rate practically down to zero. That is sure to further weaken the dollar, which has already declined in the last six weeks from about $1.25 per €1, to $1.43 per €1 (see the chart - left). And a weaker dollar means a BOOST to foreign currency translations of major global players, such as Accenture, not a negative impact.

In fact, in an interview with Dow Jones Newswires

earlier today, this writer said that,

“Global players, like IBM

(IBM), which derive most of their revenues and profits from overseas, would

benefit from low rates since they would receive an additional boost in

foreign currency translations because of the weaker dollar.”

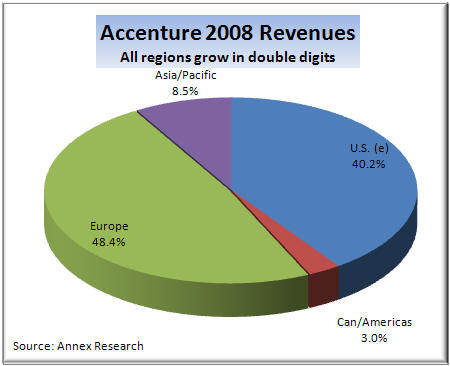

So it is not intuitively obvious to us why Accenture would be an exception. As you can see from the pie chart, the company derived last fiscal year about 60% of its business from overseas markets. So if the current trends continue and the dollar weakens further in 2009, we don't see much of a chance for significant negative currency impact.

The company's own downward revision of revenues in

local currency (9%-12% to 6%-10%) suggest s

that lower business volumes, and not the foreign currency translations, are

the major factor for a lower outlook. Accenture also lowered its

estimate of FY09 bookings from $26-$29 billion, to $24-$27 billion.

s

that lower business volumes, and not the foreign currency translations, are

the major factor for a lower outlook. Accenture also lowered its

estimate of FY09 bookings from $26-$29 billion, to $24-$27 billion.

As a result of all these downward revisions, the

company now expects diluted EPS for the full fiscal year to be in the range

of $2.78 to $2.85, down from $2.85 to $2.93. It has also lowered its

cash flow projections for the current year.

A these downward revisions taken in the aggregate may be the reason the Accenture stock barely nudged upward in after-hours trading despite the strong first quarter results. It was up only 0.33% to $30.51 (see chart - right).

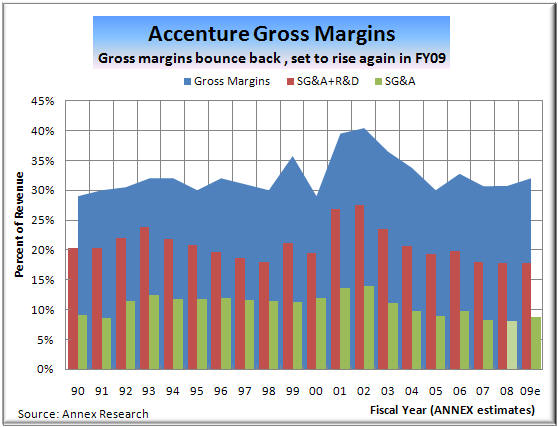

On the plus side, Accenture now expects operating margin for the full fiscal year to be in the range of 13.4% to 13.7%, up from 13.0% to 13.3% previously estimated.

Accenture's CEO Bill Green acknowledged to Reuters a "very somber, very quiet" mood among some of the company's clients. But he said the current business climate can provide opportunities for Accenture, such as growing its outsourcing business.

"There's not a board of directors out there who isn't asking the management, have you considered sourcing alternatives," he said.

Revenue increased across all of Accenture's operating groups except for financial services, its third largest, where it was flat. Green said he expects its financial services business to show strength in coming quarters, as companies work through the current trouble.

"I think it's going to hold up and then its going to break free," he told Reuters.

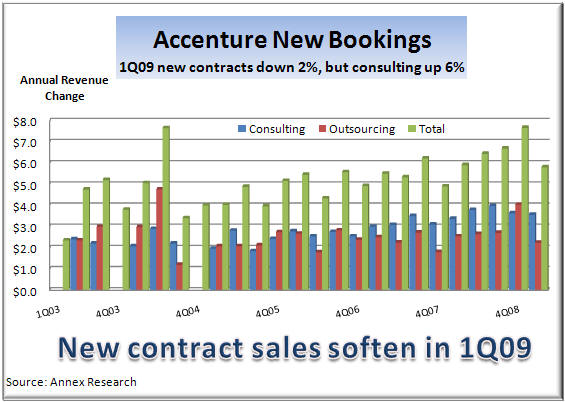

New bookings for the quarter were $5.80 billion, with consulting bookings of $3.56 billion and outsourcing bookings of $2.24 billion.

Business Segment Analysis

Revenues by Industry. Four of the five industry segments reported solid growth in the quarter, led by the Resources and Government sectors (up 16% and 11% respectively). Only the Financial Services did not grow in U.S. dollars (it was flat). But even that unit managed a 2% growth in local currencies.

· Communications & High Tech: Revenues of $1.36 billion, up 4% in U.S. dollars and 6% in local currency.

· Financial Services: Revenues of $1.24 billion, flat in U.S. dollars and an increase of 2% in local currency.

· Products: Revenues of $1.57 billion, up 6% in U.S. dollars and 9% in local currency.

· Government: Revenues of $761 million, an increase of 7% in U.S. dollars and 11% in local currency. .

· Resources: Revenues of $1,08 billion, up 16% in U.S. dollars and 20% in local currency. .

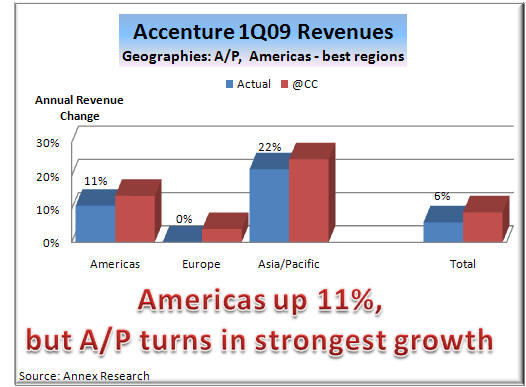

Revenues by Geographies.

Although

the Asia/Pacific region reported the highest growth, it was actually the

double digit growth in the Americas, which includes the beleaguered U.S.

market, that was the most impressive.

· Americas: Revenues of $2.58 billion, up 11% in U.S. dollars and 12% in local currency.

· Europe: Revenues of $2.87 billion, flat in U.S. dollars and an increase of 4% in local currency.

· Asia/Pacific: Revenues of $570 million, a surge of 22% in U.S. dollars and 25% in local currency.

Revenues by Horizontal Activities. Both major business segments reported solid growth, with outsourcing slightly outpacing the consulting:

• Consulting revenues for the quarter were $3.66 billion, an increase of 6% in U.S. dollars and 9%in local currency.

• Outsourcing revenues were $2.36 billion, an increase of 7% in U.S. dollars and 9% in local currency.

Summary & Outlook

New bookings are perhaps the best tangible factor in gauging a service company's future growth. And they have softened somewhat in the first quarter, down 2% to $5.8 billion. This reflects a negative 4% foreign-currency impact when compared to new bookings in the first quarter last year.

Within that total, new consulting bookings were $3.56 billion, up 6% over the year before. It was the eighth consecutive quarter of consulting bookings exceeding $3 billion.

Outsourcing new bookings were $2.24 billion, down 12% from the first quarter of last year.

So it would seem to us that the softening in demand, as reflected in lower new bookings, is the real reason behind downward revisions in Accenture's future outlook. Still, taken as a whole, the company's results stand out as a bright beacon in the sea of gloom and doom that has swept over Wall Street, especially in the last three months.

Happy bargain hunting!

Bob Djurdjevic

![]() Click

here for PDF (print) version

Click

here for PDF (print) version

![]()

For additional Annex Research reports, check out... Annex Bulletin Index 2008 (including all prior years' indexes)

![]()

Or just click on SEARCH and use "company or topic name" keywords.

Volume XXIII, Annex

Bulletin 2008-23 Bob Djurdjevic, Editor 8183 E Mountain Spring Rd, Scottsdale, Arizona 85255 (c) Copyright

2008 by Annex Research, Inc. All rights reserved. |

Home | Headlines | Annex Bulletins | Index 1993-2008 | Special Reports | About Founder | Search | Feedback | Clips | Activism | Client quotes | Speeches | Columns | Subscribe

Also check out...![]()

![]()

Accenture's "Par Excellenture" Quarter(Blowout 4Q lifts Accenture over EDS to #3 spot in IT services world)

Just Say No to Greed 2! (Proverbial IT babies being thrown out with Wall St bathwater)

"Beat the Street" Drumbeat Continues (Analysis of HP's 3Q08 business results)

Big Blue Stock Sags on "No News" Days (Analysis of IBM institutional shareholdings)

IBM Delivers Explosive Quarter (Big Blue firing on all cylinders - analysis of 2Q08 results)

MacAttack Falters at Foot of Mount Vista (A story about yet another attempt to break away from Windows)

Minting "Green" into Greenbacks (An update to our five-year forecast for IBM)

Better Late Than Never - Analysis of a rumored HP takeover of EDS

IBM "Places" By a Nose over Google - Analysis of Top 20 IT Cos stock and business performances

Big Blue Takes Chill Off Wall Street's Spring (Analysis of IBM's first quarter business results)

Just Say NO to Greed - Killer of Dreams! (An editorial comment about subprime financial crisis)

The z10 Lifts "Big Green" (Analysis of IBM's new mainframe announcement)

HP Beats the Street Again (Analysis of HP's 1Q08 business results)

Capgemini's Great Valentine's Day Gift (Analysis of Capgemini's 4Q07 and FY07 results)

Profit Drops, Stock Follows (Analysis of EDS's 4Q07 results)

Profit, Revenue Surge, Lifting Stock, Too (Analysis of CSC's 3Q08 results)

Services, Emerging Markets Boost IBM (Analysis of IBM's full 4Q07 results)

Big Blue Shines in 4Q (Analysis of IBM's preliminary 4Q07 results)

Microsoft Still Wall Street Darling (Analysis of institutional holdings of Top 10 IT Cos)