|Annex

Research | Annex Bulletins | Quotes | Workshop | Feedback | Clips | Activism | Columns

![]()

The copyright-protected information contained in the ANNEX BULLETINS is a

component of the Comprehensive Market Service (CMS). It is intended for the exclusive use

by those who have contracted for the entire CMS service.

IBM FINANCIAL

An Analysis of IBM First Quarter Results

A Disastrous Quarter!

Worse Growth Than Any under Akers: ALL Business Lines Decline! Stand by for IBM Stock to Rise...

PHOENIX, Apr. 17 - Disastrous! That’s the first word that came to mind upon our quick examination of the IBM first quarter business results, released after the markets closed today. ALL Big Blue business segments shrank! There were no exceptions this time… (software was the only line to grow slightly in the fourth quarter 2001 - see the table on and “Big Blue Stock to Take a Dive,” Jan. 17).

|

Highlights

of IBM’s 4Q01 vs. 1Q02 Business Results From

Bad to Worse… Three months ago to the day (on Jan. 17, 2002), we said: “IBM’s fourth quarter facts are now in. And they are sure to dampen investors’ enthusiasm when Wall Street opens for business tomorrow morning. In fact, the last three months of 2001 represent arguably the worst fourth quarter ever reported during Lou Gerstner’s tenure as chairman (his first full year at the helm was 1994).” And now, compare what we thought were bad 4Q01 highlights with the worse ones IBM released today:

4Q01

1Q02 · Revenue… down 11% down 12% · Net income… down 13% down 32% · Gross profit… down 9% down 15% · Americas revenue (led by the U.S.)… down 9% down 9% · Asia/Pacific… down 10% down 9% · Europe (EMEA)… down 6% down 8% · OEM… down 34% down 37% · IBM Global Services (IGS), Big Blue’s only “knight in shining armor”… down 1% (first decline ever!) down 3% · Hardware… down 24% down 25% · Global financing… down 5% down 6% · Enterprise investments… down 20% down 14% · PC revenue… down 32% down 21% · Technology revenue… down 32% down 37% …plus the unit lost money ($293M pretax) ($276M) · Software up 6% down 1% Three months ago to the day (Jan. 17), we said: “Now picture yourself as the IBM CFO

having to deliver this truckload of bad news to the marketplace.

You’d probably feel like Al Gore on September 11 -

grateful to have lost the Florida chad contest.” J

All we can add now, no wonder IBM CFO John Joyce sounded so testy and defensive during the first quarter analyst call today (Apr. 17). Yet

stand by for IBM stock to RISE tomorrow! Source: Annex Research (an excerpt from Annex Bulletin Big Blue Stock to Take a Dive?, Jan. 17, 2002) |

A testy and defensive-sounding IBM CFO, John Joyce, tried his best to put a positive spin on a bad news day. But even the best of IBM voodoo accounting magicians would have found it difficult to pull a white rabbit out of this particular black hat.

Consider the facts in IBM’s own press release. There were 24 occurrences of the words that point south; that denote bad news (decrease = 11 times; decline = 10 times; down = 3 times). The word increase was not used at all. Not even once! The term “up” figured only thrice - when IBM tried to spin the bad news by using constant currency, rather than actual numbers.

Bad press release writing? No. Bad management. Not even the best of breed news spinners cannot overcome that.

In all the years that we have been following Big Blue’s quarterly reports (which is over 30 years now), which includes the disastrous results spewed out in the waning years of the John Akers administration (1991-1992), we do not ever recall seeing such a uniformity of gloom.

So stand by for the IBM stock to RISE tomorrow. Yes, you heard us right… rise!?

Why? Because common sense and business fundamentals have long ago left Wall Street. They have been replaced by greed

and confluence of interests (between Wall Street firms/analysts/media and the companies whose stock they trade and analyze).

In such an interlocking and self-serving embrace, absence of a downside surprise is bound to be interpreted as good news. Absence of probing questions during today’s IBM analyst teleconference was proof of it.

No one took IBM to task over the $17 billion of its pension plan assets that have evaporated in the last two years (see “IBM Pension Plan Vapors: Where Did $17 Billion Go?,” Mar. 21).

No one asked why the company continues to waste its shareholders’ money on stock buybacks ($1.8 billion in the first quarter, for example) instead of investing it in GROWING the business.

No one wondered about why the former IBM CEO and all those IBM insiders sold nearly half a billion dollars’ worth of IBM shares in the last two years or so (see “Sir Lou OutLayed Lay!,” April 1).

And certainly no one quizzed IBM on why its executives are engaging in obvious conflict of interest activities, such as selling their personal stock holdings while the company they run is buying back shares.

For all above reasons,

among some others, look for “independent” analysts like that to

breathe a sigh of relief IBM didn’t trip them again, as it did last week

(see “Big

Blue Starting to Unravel,” Apr. 8).

And for the IBM stock to go up tomorrow.

Nor are you likely to find probing analyses quoted by the major financial media tomorrow. Too much (IBM) advertising revenue at risk on the one hand; and/or too much Armonk PR wrath and blackmail on the other (see “Fortune on IBM,” June 2000).

Instead, they are all likely to hail the IBM CFO for reconfirming the $4.16 per share earnings estimate for the full year. Never mind that only three months ago, Wall Street pegged IBM’s 2002 earnings at $4.81 per share. And that a year ago, security analysts expected IBM to earn $5.48 per share in this year.

Our year ago-forecast for 2002? $4.31 per share (see "IBM

Five-year Forecast: New IBM CEO to Inherit Sluggish Growth", June

19, 2001).

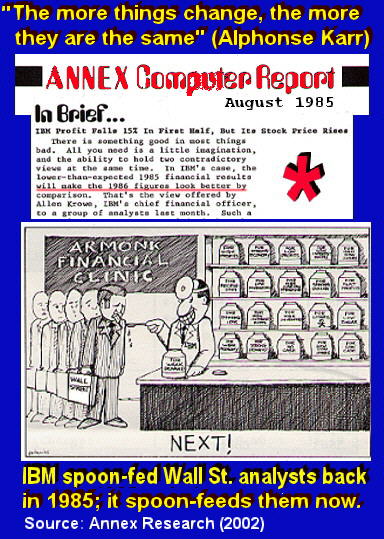

As we've noted many times before, Wall Street's memories are short, and the Big Blue skies are always bluer in weeks and months ahead (see the latest [Jan/02] example vs. an example from 15 years ago, and the “Armonk Financial Clinic” [above] cartoon from 17 years ago).

So

rather than chastise IBM for blowing its own forecasts and Wall Street's

expectations by at least 24% since last year, they are applauding IBM for

meeting their scaled-down estimates.

We

used to refer to Wall Street of the 1990s as a casino.

Strike that. Make it a

bordello in the early 2000s. Or

a casino with a bordello on the side, if you prefer.

“Independent” Analysts?

Too strong a characterization? Well, you be the judge…

In advance of today’s IBM release, we did a little checking about the so-called “consensus,” the almighty gauge of relative health of a public company’s earnings. In IBM’s case, of the 21 analysts surveyed by Thompson Financial, 14 still continue to recommend the stock as a “strong buy” or a “buy.” Seven have a “hold” on it. None, not a single analyst, has a “sell” or “strong sell” on IBM!

Meanwhile, Big Blue shares have lost over $70 billion (or a third) of their market value in the last three months alone! (they dropped from about $126 in January, to about $84 today).

In fact, we’ve noticed something rather comical about Wall Street analysts’ IBM forecasts. During the next 12 months, the highest “high target” price predicted by the analysts surveyed by Thompson Financial was $140. The lowest “low target” price was $90.

As you saw, IBM traded today as low as $84. In other words, we are already below the lowest “low target” price, yet the analysts still keep predicting great things for IBM.

Enron anyone?

As for our own outlook, here is what the CBS Market Watch published today BEFORE the IBM earnings were released:

"They're

probably going to say that the track is still muddy, but we're still ahead

of the pack, and that's anything but the truth," said Bob Djurdjevic,

analyst with Annex Research in Phoenix. "When you compare IBM with

the industry, the company's earnings will be down about 31 percent from

the year-ago period, while the entire sector will be down about 1

percent."

And what happened? IBM earnings were down 31%. The IT industry tallies are still coming in. And yes, Big Blue did say in the release that, “IBM continued to outpace the competition.”

“We remain confident about the fundamental strength of our business and about our prospects of the future,” said IBM’s new CEO, Sam Palmisano.

Wish his former boss were as confident. Lou Gerstner wouldn’t have dumped $424 million of IBM shares before riding into the sunset, headed for golf courses (see “Sir Lou OutLayed Lay!,” April 1).

The

only thing missing from IBM s "color commentary" was the muddy

track. We put it in as our own metaphor.

J

Segment

Analysis

Since we summarized all the “gory details” of

IBM’s first quarter vs. fourth quarter business results in the “From

Bad to Worse” table), we will drill down on only one aspect of it -

IBM’s “customer deferral” explanations for the low demand for its

products and services.

It is now quite clear that Joyce/IBM appear to have

misled the market when he said in January that the fourth quarter results

were down because of some contract signing deferrals (see "Grand

Slam-Dunk of Bunk," Jan. 18, 2002).

Here’s an excerpt:

“When Joyce pulled the same stunt two years ago, blaming the IBM woes on the Y2K that time, we called it a “Slam-Dunk of Bunk,” (Jan 19, 2000). This afternoon, Joyce has outdone himself. Make it a “Grand Slam-Dunk of Bunk!” [...]

Everybody knows that service contracts are annuities; that revenues are usually earned over a five to 10 year-contract period. Everybody also knows that it usually takes six to nine months for a mega-contract to start to produce revenues and profits for a vendor. So the fourth quarter contract signings ($15 billion, according to IBM) could not have been reasonably expected to contribute much to the company’s top and bottom lines until well into 2002.

Unless,

of course, the Big Blue is into something it is not supposed to be in -

such as “aggressive accounting” - booking revenue and earnings early

(for more on that, check out the “Enronizing IBM?” part of this

report).”

The

IBM CFO must have heard or read about our assessment, because he had a new

explanation today. Joyce

whipped up some new charts which showed how IBM supposedly again lost

important sales due to customer deferrals in the last two weeks of first

quarter (see Slide

6 at the IBM web site).

Oh,

shucks… such bad luck!

And for two quarters in a row… Anyone has a spare quarter to give

to IBM as consolation? J

As the Dow Jones Newswire put it in a subsequent article:

"While investors cheered IBM's first-quarter report and its outlook, Bob Djurdjevic, an analyst at Annex Research in Phoenix, and an outspoken critic of IBM, said his first reaction to the results was "disastrous."

Everything that matters is

down...literally," he said. "Now that all IBM business lines

continue to point south, IBM continues to talk about 'deferred purchases'

and blue skies ahead."

Meanwhile,

no one in the esteemed analyst audience asked the IBM CFO whatever

happened with those fourth quarter deferrals.

If they were just a temporary aberration, as IBM implied,

shouldn’t they have spilled over into the first quarter?

And if so, why does it matter if some new deferrals occurred that

offset the fourth quarter benefit?

More importantly, no one challenged Joyce about another new chart, shown for the first time during this afternoon’s IBM analyst call. The graph depicts IBM Global Services (IGS) revenue vs. its new contract signings’ growth (see Slide 12 at the IBM web site).

The IBM CFO used it to show that, now that we’ve two successive quarters of growth in new contract sales, the IGS revenue growth is supposedly just around the corner (IGS revenue declined 3% in the first period).

Apart from a frail argument that a growth RATE increase, rather than absolute value of new contract signings, drives the revenue, we were stunned by an implied statement: Since the second quarter of 2000, IGS had had FIVE CONSECUTIVE QUARTERS of DECLINING new contract sales.

Yet this has never been disclosed overtly by IBM till now. Instead, we were being told, quarter-after-quarter, how great IBM new contract sales had been. Which is why we kept wondering how it was possible for IGS new sales to be strong and revenues to be flat or declining? (see “EDS: What Recession?”, Feb. 8).

Now we know. IBM didn’t give us the bad news except in hindsight, as contrast to the good news figures from the last two quarters. And even now, its explanation only skirts and obfuscates the real reason.

We think that the main reason IGS revenues kept declining despite good new contract sales is that IGS expirations and cancellations were too high.

As you can see from the chart, IGS has sold about $121 billion in new business since 1999, while its backlog increased by only $48 billion during that time frame. This implies that about $73 billion of the new contract sales was offset by expirations and cancellations.

But that’s NOT what either the IBM CFO volunteered to talk about, nor what any Wall Street analyst asked.

As we said, a bordello…

And thus a good place to stay away from. A real Las Vegas casino would probably be far less expensive.

Happy bargain hunting!

Bob Djurdjevic

P.S. (Apr. 18, 2002): The IBM stock

went up over four points today to close at $89! J