Annex Bulletin 2009-08 May 1, 2009

A partially OPEN edition

Recent... ![]()

Back on Growth Track - Analysis of IBM Global Services 2008 results

Sometimes Less Is More and Down Is Up - Analysis of IBM's 1Q business results

IT SERVICES

Updated 5/03/09, 11:30PM PDT

Analysis of IBM Global Services' 2008 Business Results

Back on Growth Track

Services Now Again Boost IBM's Revenue and Profit Growth Rates; But First Quarter Shows Some Clouds on Horizon

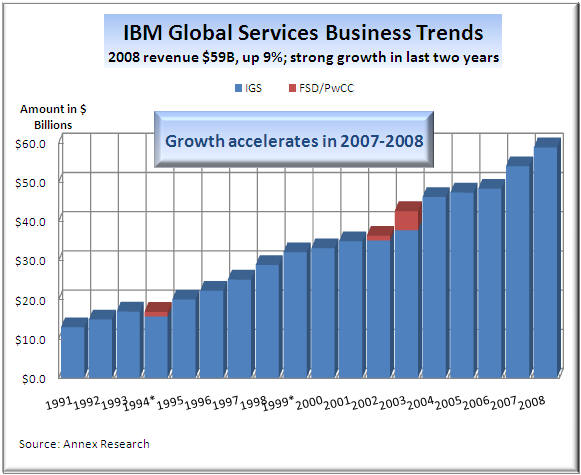

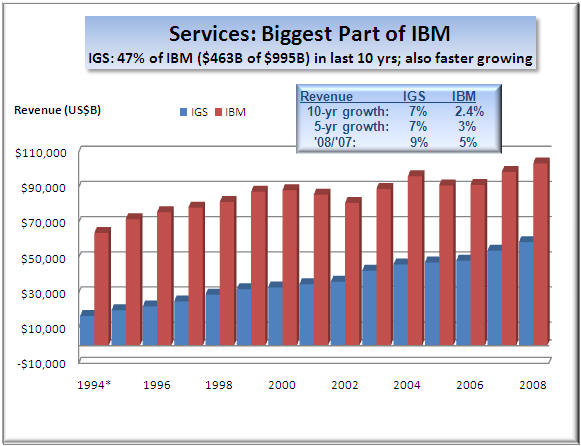

HAIKU, Maui, May 1 – One rarely sees in business or in life that the biggest entity is also the fastest growing. IBM Global Services is evidently an exception to this general rule of thumb. At $59 billion in annual revenue, Big Blue's services arm is several times larger than most of its top competitors. In 2008, it has also grown faster than most, and more rapidly than IBM as a whole.

Our analysis of IGS's 2008 business results shows an operation whose steady growth (left chart) has accelerated in the last two years, as several of its major competitors began to sputter, after slowing down in 2005-2006 and 2000-2002 periods. As a result, IBM's two services units - Global Technology Services (GTS) and Global Business Services (GBS) have resumed their leadership position within Big Blue's lines of business.

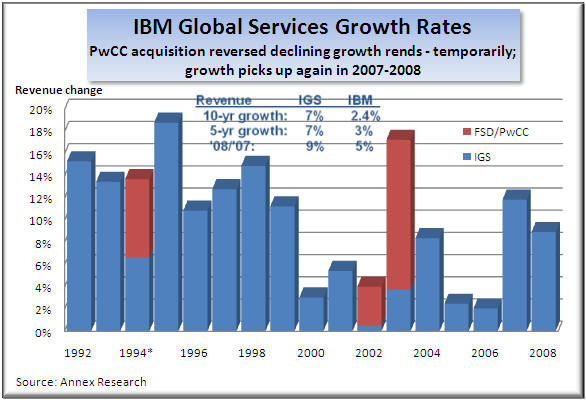

In 2008, they have outpaced IBM's corporate revenue grown 9% to 5%. For the last five years, they have grown at 7% versus IBM's 3% overall compound annual growth. And in the last decade, they have outpaced the corporation 7% to 2.4% (middle chart).

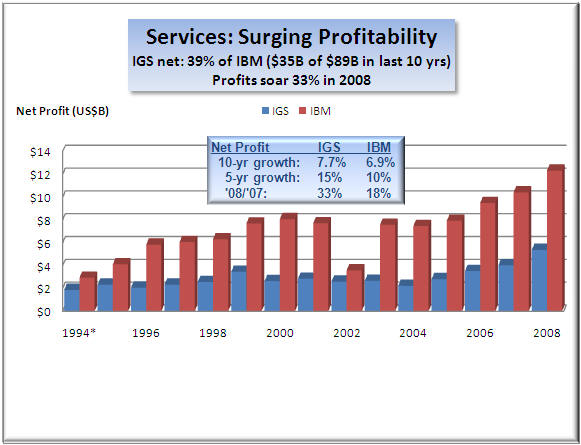

More importantly for IBM shareholders, IGS has outpaced Armonk's corporate profitability growth by an even greater margin during the same periods. Last year, IGS' estimated net earnings grew by 33% over the year before, versus IBM's (impressive) 18% overall surge, despite a global economic slowdown. During the last five years, IGS led by 15% versus 10%. And in the last decade, IGS's profits outpaced IBM's 7.7% to 6.9% compounded annually, despite some hard times in the 2001-2004 time frame (right chart).

What Changed?

So long gone are the times from the mid- to late 1990s when services boosted IBM's revenues while being a drag on Big Blue's earnings. What has changed since then?

Well, the biggest change was that today IBM has a leader whose focus is on improving the quality of his operations rather than quantity. In the services business, that translated into doing things more efficiently and at lower cost while keeping an eye on the top line, too.

IGS certainly cannot claim

to be the first to apply the "reusable assets" concept (or "service

products," as IBM calls them) to the way it does business (see

IBM:

Services in a Box , Sep 2006). But it has

certainly been more consistent in that respect than some other vendors.

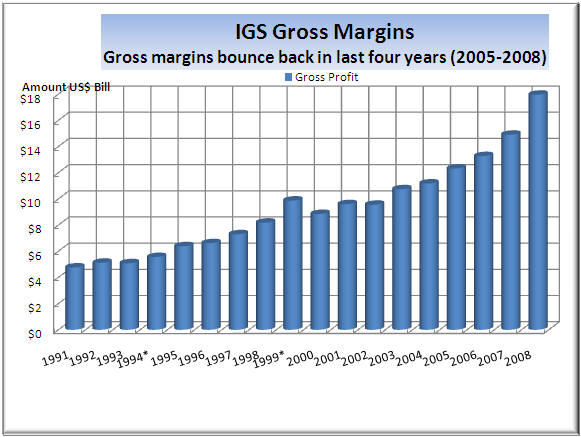

As results, IBM services' profit margins have been growing both at the gross

and pretax levels.

2006). But it has

certainly been more consistent in that respect than some other vendors.

As results, IBM services' profit margins have been growing both at the gross

and pretax levels.

IBM also has a unique advantage over its other major global services competitors. It can and does use its software and hardware divisions' products as a unique way of packaging its integrated solutions, especially for large enterprise customers. In the case of GTS, for example, IBM hardware and software accounted for about $2 billion as compared to $30 billion of the "pure" services revenue in 2008. More importantly, some of these services deals might not have happened without the advantages that IBM's software and hardware solutions provided.

As a result, new business signings, for example, were very strong in the fourth quarter of last year. In the midst of the deepest recession the world has seen since the Great Depression they were up 20%. GBS (consulting) sales weren't as strong, as long-term engagements contracted 18% for the year. Obviously, customers have been putting more emphasis on execution and immediate savings than on long-term planning and strategic transformations.

Finally, IBM's holistic approach on treating businesses as living organisms rather than a conglomeration of individual parts has been reflected in its global services strategy (see IBM's Holistic Approach - secret of success, Feb 2009).

Summary & Outlook

During the last 10 years, IGS

has emerged as not only the penultimate giant of the global ser vices

industry, but also as the largest part of Big Blue by far. Services

accounted for about $463 billion or 47% of IBM's $995 billion total

revenues. This portion of the company now accounts for over 60% of the

total. And given the faster growth than the rest of IBM's parts,

IGS's share of IBM's business is likely to continue to increase in the

future, too.

vices

industry, but also as the largest part of Big Blue by far. Services

accounted for about $463 billion or 47% of IBM's $995 billion total

revenues. This portion of the company now accounts for over 60% of the

total. And given the faster growth than the rest of IBM's parts,

IGS's share of IBM's business is likely to continue to increase in the

future, too.

But if the first quarter

results are an indication, it is not going to be smooth sailing all the way.

For, IGS revenues

decreased 10% (down 2% in constant currency). Global Technology Servi ces

(GTS), the outsourcing and infrastructure services provider, shrank to $8.8

billion in revenu

ces

(GTS), the outsourcing and infrastructure services provider, shrank to $8.8

billion in revenu es.

Global Business Services (GBS) declined to $4.4 billion.

es.

Global Business Services (GBS) declined to $4.4 billion.

IBM signed new services contracts totaling $12.5 billion in the first quarter, a drop of 1%. But the backlog was down by more than $4 billion to $126 billion, compared with $130 billion at year-end 2008. And that could spell trouble down the road.

For, when the outflow of business from the backlog exceeds the inflow of new deals, what follows is a drop in revenues. So the revenue declines IGS is now experiencing are a consequence of a negative backlog trend that started in 2008, and has evidently now extended into 2009 (see above charts).

The only remedy to this problem is for IGS to sell more and lose less. And that's easier said than done, especially in current economic conditions. Yet, playing tough defense (shoring up renewals and stemming the outflow of deals) is the only way IGS will get back on the growth track and resume its leadership position within IBM.

|

Annex Clients: CLICK HERE for detailed IGS 2008 P&L tables & charts |

Bob Djurdjevic

![]() Click

here for PDF (print) version

Click

here for PDF (print) version

![]()

For additional Annex Research reports, check out... Annex Bulletin Index (including all prior years' indexes)

![]()

Or just click on SEARCH and use "company or topic name" keywords.

Volume XXIII, Annex Bulletin 2009-08 Bob Djurdjevic, Editor 894 E Kuiaha Rd, Haiku, HI 96708; Tel/Fax: +1-602-824-8111

(c) Copyright 2009 by Annex Research,

Inc. All rights reserved. |

Home | Headlines | Annex Bulletins | Index 1993-2009 | Special Reports | About Founder | Search | Feedback | Clips | Activism | Client quotes | Speeches | Columns | Subscribe

Also check out...![]()

![]()

IBM's Holistic Approach - Treating businesses like living organisms - secret of success

IBM Tries to Pull Dow, HP Up - Big Blue stock up sharply after CFO remarks at investor conf

Hurd's First Stumble - HP's 1Q09 revenues, earnings disappoint Wall Street

Two Thumbs Up for Big Blue - Analysis of IBM 4Q08 business results

Big Blue: All Heart - IBM creating new jobs in American Heartland

When You Catch a Tiger by the Tail... - An editorial about greed & success

Squeezing the Consumer Dry (Greed fueled both bankers & oilmen's try to squeeze blood out of stone - consumer)

The Year of Living Dangerously - Analysis of global investment trends