Annex Bulletin 2009-13 July 13, 2009

A partially OPEN edition

Recent... ![]()

Revenues, Earnings Drop - Analysis of Accenture's 3QFY09 business results

IBM Wins the "Gold" - Analysis of IT Services Octathlon 2009 results

INDUSTRY TRENDS

Updated 7/13/09, 12:15PM HIT

Analysis of Top Global IT Companies' Market & Business Performance

Apple, Google Pace Comeback

Sun Shines Again, But Only at Oracle; Microsoft, IBM Hold Top Market Cap Positions; HP Slides Down to #7

HAIKU, Maui, July 13 –

What a difference just half a

year can make! Six months ago, we called 2008 a "year of carnage."

Our year-end analysis of Top 19 IT companies' stock and business

performances -

"Mr. Murphy's Year" Mercifully Ends

- showed a 38% drop in market cap since the spring of last year.

Now the aggregate market cap of the same companies is back to over one

trillion dollars, up 20% since the start of the year.

Good news? It could be, if the market prices were driven up by solid

business performances. Alas, that's not the case. The same Top

19 comp anies'

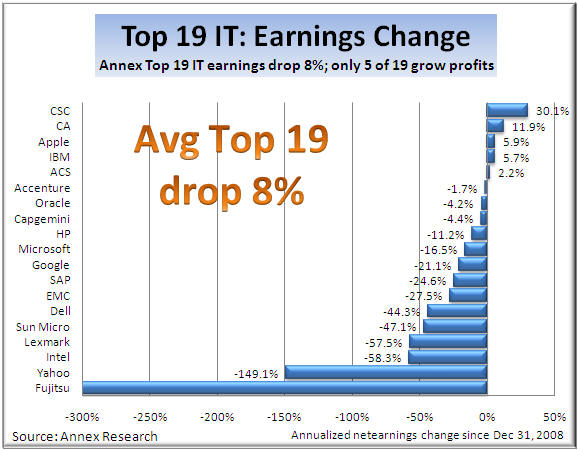

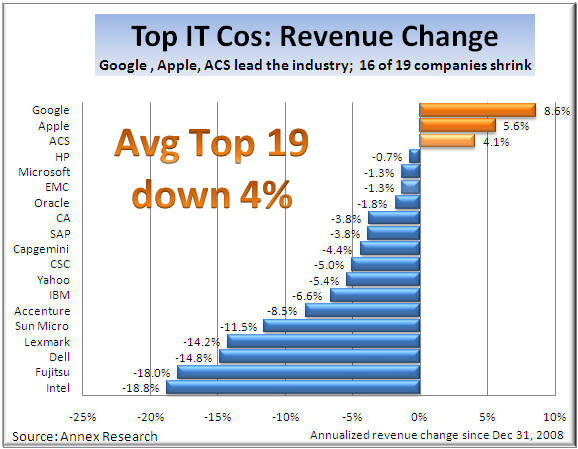

annualized revenues were down 4% in the last six months, while their

earnings slumped 8% during the same time frame (right charts).

anies'

annualized revenues were down 4% in the last six months, while their

earnings slumped 8% during the same time frame (right charts).

"High tides lift all boats," they say. That's certainly true on

Wall Street. So appears that the stock market's increases were fueled more by hopes and prayers than by

strong

revenues and earnings. Business facts do not back market perceptions.

stock market's increases were fueled more by hopes and prayers than by

strong

revenues and earnings. Business facts do not back market perceptions.

Of course, that's not unusual on Wall Street. In the second half year, for example, the same Top 19 companies reported solid revenue and earnings growth (up 6%), yet their stocks got clobbered (down 38%, as you saw above). So maybe the market is now correcting its negative overreaction last year?

MARKET Rankings of Annex Top 19 IT Companies

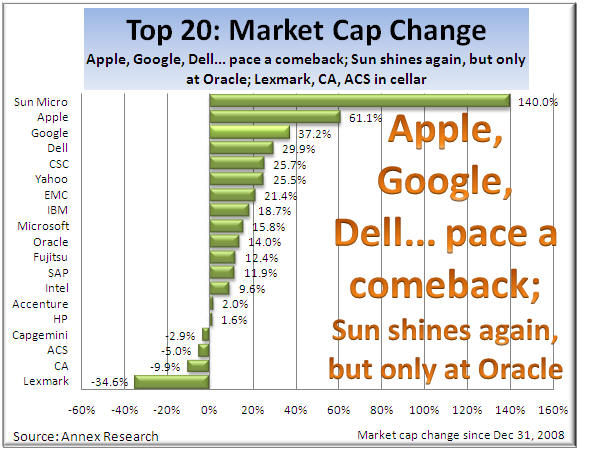

Market cap. Meanwhile, Microsoft and IBM are still No. 1 and No. 2 in market cap respectively. Both companies' values increased in double digits - up 16% an 19% respectively - since the year end. But Google, the No. 3, saw its market cap grow faster. It is up 37% since Dec 31, narrowing the gap between itself and Big Blue.

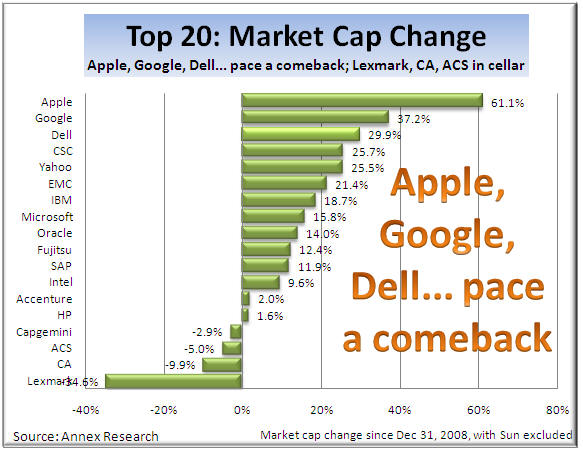

Meanwhile, Apple, the No. 4, made the biggest jump. It leapfrogged over HP, Intel and Oracle on the heels of a 61% surge in its market cap. It was the best stock performance among the Top 19, excluding Sun Micro, whose market cap surged 140%. But it was a swan song. The stock rose that much solely on the basis of Oracle's acquisition of a former highflyer in the Unix arena. Which is why we are showing you the Market Cap Change chart with (middle) and without Sun Micro (right).

It is also worthy of note that Dell, Yahoo and EMC shares also recorded strong performances in the first half of the year, rising in the 25% to 30% range. The three companies exemplify and accentuate the dichotomy in the current market. For, their earnings DECLINED in double digits during the same time frame. Evidently, Wall Street sees something in these companies we don't.

At the other end of the market cap scale, Lexmark, CA and ACS are holding up the rear. All three companies' market values declined in 2009 to-date. But they were an exception. For, 15 out of the Top 19 stocks experienced increases, a sharp turnaround from the second half of 2008 when ALL top IT companies saw their market caps shrink.

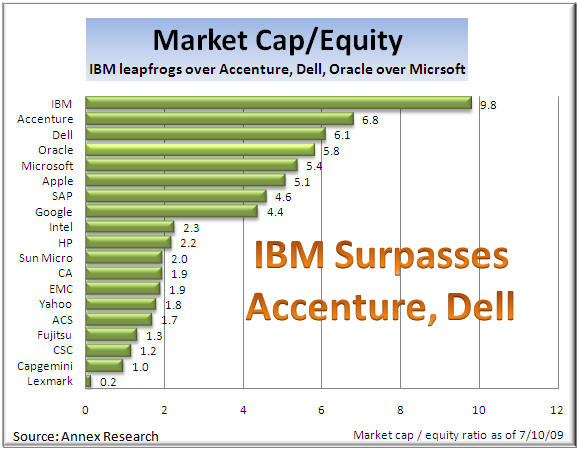

Market cap/equity.

The Market Cap over Equity ratio - the "fluff ratio" as we called

it over a deca de

ago - tends to reflect Wall Street's views of future earnings rather than

"money in the bank" (actual shareholders equity). After 15 years of

incessant buybacks, Big Blue has depleted its equity to the point that it is

now the industry leader in Market Cap/Equity ratio.

de

ago - tends to reflect Wall Street's views of future earnings rather than

"money in the bank" (actual shareholders equity). After 15 years of

incessant buybacks, Big Blue has depleted its equity to the point that it is

now the industry leader in Market Cap/Equity ratio.

Accenture, Dell, Oracle, Microsoft and Apple follow, in that order. Lexmark, Capgemini, CSC and Fujitsu are at the bottom of the rankings.

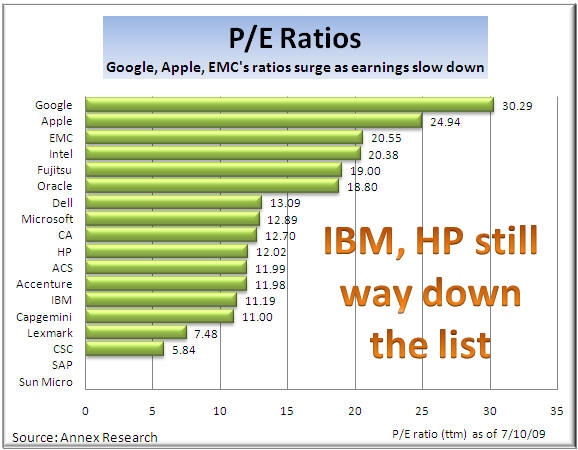

P/E Ratio.

Price/Earnings (P/E) ratios also measure expected profits implied in

the stock price ve rsus

actual earnings. Once again, Google and Apple are at the top of the

stack, followed by EMC and Intel.

rsus

actual earnings. Once again, Google and Apple are at the top of the

stack, followed by EMC and Intel.

Having a high P/E ration is not necessarily a sign of great business health. Apple was the only company among the four to actually report a growth in earnings. The other three saw their profits drop, Intel's and EMC's quite sharply (down 58% and 28% respectively). So even modest stock prices increases can mean high P/E ratios if the earnings decline even faster. To us, a high P/E ratio is a warning sign that perhaps the stock may be overinflated.

BUSINESS Rankings of Annex Top 19 IT Companies

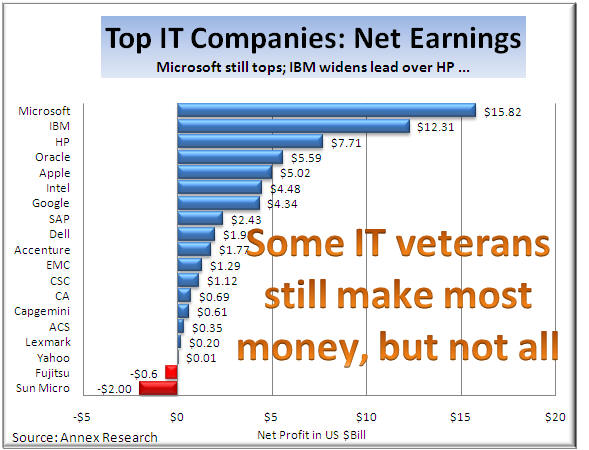

Net Earnings.

Some global IT industry veterans are still making the most money, market turmoil and recessions notwithstanding.

Microsoft, IBM, HP and Oracle top the list of the Top 19 global competitors

when it comes to net earnings. But not all old-timers are that

fortunate. At the other end of

the spectrum, other computer making geezers, like Fujitsu and Sun Micro,

are spewing out red ink.

At the top, Microsoft's lead over IBM has shrunk a little, while the gap between IBM and HP, the No. 3 in the rankings, has widened since the last time we did this analysis.

Apple has now

leapfrogged over Intel, while Google, a relative newcomer, is nibbling at

the old IT chipmaker's heels.

On the other hand, Yahoo, however, another relative upstart like Google, finds itself in the cellar, after just barely breaking even at the bottom line in recent times.

Another sign of the times is that only five of 19 companies actually reported a growth in annualized earnings in the last six months (left chart). As a group, their average profits have shrunk 8% during that time frame.

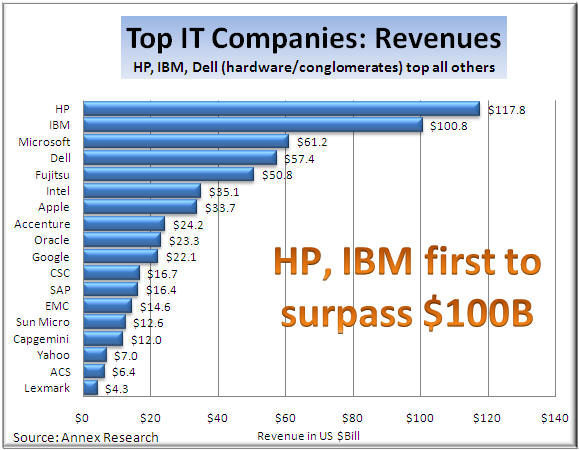

Revenues.

HP and IBM continue to rank as the No. 1 and No. 2 global IT

competitors respectively in terms of revenues. There is a wide gap of

over $40 billion between them and Micros oft

(No.3) and Dell (No. 4).

oft

(No.3) and Dell (No. 4).

Other hardware makers, such as Fujitsu, Intel and Apple are in the next

tier. So one could conclude from the above that the size still matters

when it comes to manufacturing. Alas, Lexmark and Sun Micro, for

example, at the bottom of the list, serve to discount that theory.

The chart on the right, depicting the annualized revenue changes in the last six months, accentuates that point. Here you have Google, Apple and ACS on top, and Intel, Fujitsu, Dell, Lexmark and Sun (all hardware vendors!) at the bottom of the ranking.

But as a group, the Top 19 revenues declined 4% on an annualized basis as 16 of the 19 competitors' revenue shrank.

So size only matters if you can use it to generate more profits or faster top line growth that actually drops to the bottom line. And that's becoming increasingly more of an exception than a rule in the IT industry. "Small is beautiful" seems to be the name of the game these days. That's what the above charts seem to be telling us.

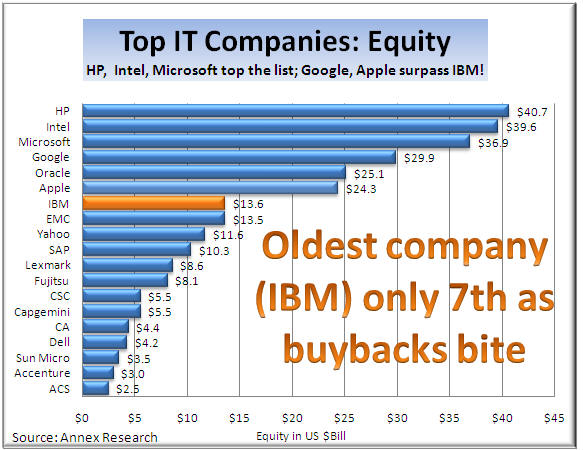

Equit y.

All other things being equal, the older the company, the higher

its equity should be. Sure enough, HP, Intel and Microsoft, three of

the veterans in the IT industry, are at the top of the equity rankings.

y.

All other things being equal, the older the company, the higher

its equity should be. Sure enough, HP, Intel and Microsoft, three of

the veterans in the IT industry, are at the top of the equity rankings.

But all other things are not equal. So IBM, by far the oldest company in the industry, is only seventh in terms of equity, having been surpassed by Apple, Oracle and Google since our last report. Such as is the price of stock buybacks, the path that Big Blue has been on since the mid-1990s. So rather than keep most of its wealth within the company's balance sheet, IBM and others have been dispensing cash through share repurchases to some of its holders.

Summary: Market Up, Business Down

We seemed to be right now at a peculiar junction in time when the market pendulum is swinging up while the business indicators are pointing down. Which is the "correct" direction? When will the two gauges get back in balance?

The next few weeks will provide additional clarity about those questions as the second quarter earnings season is upon us. On Thursday, IBM reports its second quarter results. Based on what we have seen from HP in May (Suddenly, All Lines Point South) and Accenture in June (Revenues, Earnings Drop ), it is a difficult time in the IT industry.

|

Click here for detailed tables and charts (Annex clients only) |

Bob Djurdjevic

![]() Click

here for PDF (print) version

Click

here for PDF (print) version

![]()

For additional Annex Research reports, check out... Annex Bulletin Index (including all prior years' indexes)

![]()

Or just click on SEARCH and use "company or topic name" keywords.

Volume XXIII, Annex Bulletin 2009-13 Bob Djurdjevic, Editor Tel/Fax: +1-602-824-8111

(c) Copyright 2009 by Annex Research,

Inc. All rights reserved. |

Home | Headlines | Annex Bulletins | Index 1993-2009 | Special Reports | About Founder | Search | Feedback | Clips | Activism | Client quotes | Speeches | Columns | Subscribe

Also check out...![]()

![]()

Suddenly, All Lines Point South - Analysis of HP's 2Q09 business results

Back on Growth Track - Analysis of IBM Global Services 2008 results

Sometimes Less Is More and Down Is Up - Analysis of IBM's 1Q business results

IBM's Holistic Approach - Treating businesses like living organisms - secret of success

IBM Tries to Pull Dow, HP Up - Big Blue stock up sharply after CFO remarks at investor conf

Hurd's First Stumble - HP's 1Q09 revenues, earnings disappoint Wall Street

Two Thumbs Up for Big Blue - Analysis of IBM 4Q08 business results

Big Blue: All Heart - IBM creating new jobs in American Heartland

When You Catch a Tiger by the Tail... - An editorial about greed & success

Squeezing the Consumer Dry (Greed fueled both bankers & oilmen's try to squeeze blood out of stone - consumer)

The Year of Living Dangerously - Analysis of global investment trends