|Annex

Research | Annex Bulletins | Quotes | Workshop | Feedback | Clips | Activism | Columns

![]()

The copyright-protected information contained in the ANNEX BULLETINS is a

component of the Comprehensive Market Service (CMS). It is intended for the exclusive use

by those who have contracted for the entire CMS service.

IBM FINANCIAL

An

Analysis of IBM Insider Stock Trading in 2000-2001

Sir Lou OutLayed Lay!

Outgoing Chairman of “IBM Greed, Inc.” Dumped About $238M of Big Blue’s Stock in Last Two Years While Hyping Up Big Blue’s Bright Future

PHOENIX,

Apr. 1 - Move over Ken Lay, Sir Lou is here.

Lou Gerstner, IBM’s outgoing chairman (see Gerstner's

Legacy: Good Manager, Poor Entrepreneur, Jan. 29), is the new

candidate for Wall Street’s King of Greed title. In the “hype and sell” competition, Sir

Lou easily outLayed Lay, former Enron chairman - by more than

four-fold (not an April Fools’ Day joke! J).

PHOENIX,

Apr. 1 - Move over Ken Lay, Sir Lou is here.

Lou Gerstner, IBM’s outgoing chairman (see Gerstner's

Legacy: Good Manager, Poor Entrepreneur, Jan. 29), is the new

candidate for Wall Street’s King of Greed title. In the “hype and sell” competition, Sir

Lou easily outLayed Lay, former Enron chairman - by more than

four-fold (not an April Fools’ Day joke! J).

In 2001, for example, Lay and six other top Enron officers unloaded some $175 million of the company stock for a pretax gain of about $130 million (click here for details).

When the news of these Enron insider trades broke in late January, it was greeted with astonishment by the media. The Knight Ridder Tribune, for example, said in a Jan. 25, 2002 story the “stock-selling spree was extraordinary even by the standards of the aggressive energy-trading industry.”

Well, Enron’s insider sales were small potatoes compared to Big Blue’s. The latest SEC form 144 filings show that its outgoing chairman alone dumped more stock in the worst year of IBM growth (read decline) during his tenure at the Big Blue helm than did all top seven Enron executives - combined! (see Big Blue Stock to Take a Dive?, Jan. 17).

In 2001, Gerstner sold about $159 million worth of his IBM holdings for an estimated pretax gain of about $133 million[i]. In the last two years, he unloaded about $238 million of the IBM stock for an estimated pretax gain of about $197 million.

Since the start of the IBM insider selling spree in late 1996, Gerstner has disposed of nearly half a billion dollars’ worth of IBM shares (about $424 million) for an estimated pretax profit of about $345 million (see "Some Insiders Cashed in on IBM Stock Buybacks", May 1997, “Executive Suite: How Sweet!,” July 1997), "Where Armonk Meets Wall Street, Greed Breeds Incest", Nov. 1998, and "Gerstner: Best Years Are Behind", Aug. 10, 1999).

According to the IBM Proxy Statements, Gerstner’s total compensation in the last five years was $366 million, of which 83% or $302 million was generated by insider stock sales (see IBM Greed, Inc., and LVG Greed, Inc. tables).

By contrast, Lay’s and Jeff Skilling’s (former Enron CEO) aggregate stock sales between October 1998 and November 2001 were “mere” $101 million and $67 million respectively (see the Washington Post, Jan. 27, 2002 and Sir Lou Easily Outlayed Lay).

Now, how about that, Ken Lay and Jeff Skilling?! Unseemly actions of the former chairman of “IBM Greed, Inc.” CEO put the Enron boss and his top lieutenants self-enriching efforts to shame even by the standards of the Wall Street House of Shame(lessness).

Yet, there has been not a peep about it in the major media or from Wall Street analysts. Just as they stayed mum last fall about Enron. Which aided and abetted the top Enron officers’ deceit of their shareholders and employees.

But there were some honorable exceptions. The “Insider Selling by Enron Execs Speaks Louder Than Their Words,” for example, was published by TheStreet.com on July 20, 2001, even before Lay and Skilling completed their selling spree. Here’s a summary:

“The two

executives (Lay and Skilling - Annex Ed.)

"have a long record of creating and sustaining value for

shareholders. I have a high level of confidence that Skilling can

continue that record," McIntyre (an analyst - Annex Ed.)

said.

But appearances

count. "It's a question of perceptions," says McIntyre.

"In this market, anything can get a company, and the insider-sales

news does hurt."

That's especially true when actions and words don't mesh. As the analyst quipped, "It's what they call an oxymoron. You are saying one thing and doing another".”

Sound familiar? Just substitute Gerstner for Lay, and IBM for Enron, and you may see that Sir Lou is afflicted with a more aggressive Big Blue strain of Enronitis.

When the roof fell in with Enron’s Chapter 11 filing on December 2, the heretofore kow-towing media suddenly “discovered” the Enron scams, and started throwing stones at the former Wall Street darling. Here’s one example (again, quoting from that Knight Ridder Jan. 25 article):

“Much criticism has already been leveled at Lay, Enron's chairman, for selling huge quantities of Enron stock and then a few weeks later urging Enron employees to buy it. In e-mail exchanges with Enron employees on Sept. 26 - about eight weeks after his last recorded stock sale on July 31 - Lay encouraged his company's workers to "talk up the stock and talk positively about Enron to your family and friends."

While

there is no indication that the many insider sales at Enron last year

were illegal, experts said the volume and the value of the sales raise

serious ethical questions.”

Again, just as in IBM’s case. Only worse, when it comes to Armonk’s insider trades.

Now, as we’ve said

before (see Enronizing

IBM, Jan. 17), we do not expect IBM to file for bankruptcy any time

soon. But “something is

rotten in the state of Denmark Armonk” (Hamlet), judging by

IBM’s silence about the $17 billion that seem to have disappeared from

its pension fund assets in the last two years (see IBM

Pension Plan Vapors: Where Did $17 Billion Go?, Mar. 21).

As you saw from the above Annex Bulletin, we had written to the SEC chairman, Harvey Pitt, pointing out our $17 billion quandary and IBM’s unwillingness to respond to our questions. Last week, we got a call from the SEC, responding to our correspondence. It suffices to say that if the SEC does its job, IBM will be getting some more questions soon.

Pay for Performance? Not at Armonk’s Boardroom!

Meanwhile, back at IBM

Greed, Inc., as best as we can trace it, Gerstner’s self-aggrandizing

and self-enriching scheme started in early 1995.

After having appointed some of his cronies to the IBM Board’s

Executive Compensation Committee (Charles Knight [Emerson] and Charles Vest [M.I.T], who were joined later by Ken Chenault [AmEx]),

the IBM chairman, a former AmEx CEO, has been showered with generosity

even for meager results.

and Charles Vest [M.I.T], who were joined later by Ken Chenault [AmEx]),

the IBM chairman, a former AmEx CEO, has been showered with generosity

even for meager results.

Here’s an excerpt about it from a Mar. 14, 1995 New York Times story, “A Good Year for Big Blue and Its leaders”:

“The turnaround last year was modest,”

said Bob Djurdjevic, president of Annex Research, a Phoenix computer

research and consulting firm. “I

think that Gerstner has done some very good things, but I’m not sure

that the chairman’s compensation should run that far ahead of the

company.”

It was a tell-tale sign of things to come. For, IBM chairman’s salary has continued to run ahead of the company’s performance throughout his nine-year tenure at Armonk. Gerstner’s cozy arrangement with his old pals, whom he appointed to the Board, made a mockery of the famous old IBM culture principle - “pay for performance.”

But they saved the worst for the last (year as CEO).

Take a look at the Appendix A of this Bulletin to find out how Sir Lou did in 2001. The four members of the IBM Executive Compensation committee try to justify why they awarded to the IBM chairman $128 million in 2001, according to the IBM Proxy Statement (or even quite a bit more than that, as you saw by our figuring of the pretax gain from stock sales). But the foursome end up sounding lame.

Then take a look at Appendix B to see how IBM did in 2001 (after the latest fourth quarter results).

Hopefully you will conclude what we also surmised - that the company’s results had no bearing whatsoever on the IBM CEO’s compensation. Gerstner’s cronies on the IBM Board awarded the lackluster former IBM chairman a huge sash of cash and stock merely as a farewell “you scratch my back, I’ll scratch yours”-gesture.

No surprise there. Here’s what this writer said in the Global Technology Business column “Five More Years…” (Dec. 1997):

“Those who think that GREED and

VANITY are acceptable principles upon which to run IBM for another five

years, should contemplate what eventually happened to the former masters

of the Louvre AND of Versailles. Moral

of the story? Money and technology will never be a substitute for ETHICS

and MORALITY! Which is why a resounding "yikes" was this

writer's reaction to five more years of Gerstner.”

“Good

riddance!” is what many Big Blue shareholders might say as a farewell

to a Big Blue leader who used IBM as his personal cash cow, siphoning

off about $366 million in the last five years alone.

“Good riddance!” is what many shareholders may also want to say to the IBM directors who made Gerstner’s “hype and sell” game possible. They shirked their fiduciary duty to shareholders in favor of loyalty to the man who put them on the IBM Board.

“Good riddance!” is what Big Blue’s top insiders implicitly said when they dumped huge amounts of IBM stock last year (chart).

SUMMARY

What happened at Enron, Global Crossing, etc. may come as a surprise to some investors, as these companies’ bubbles burst rather suddenly. But what is happening at IBM is proof that greed and moral corruption are endemic in corporate America.

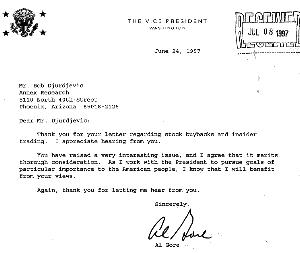

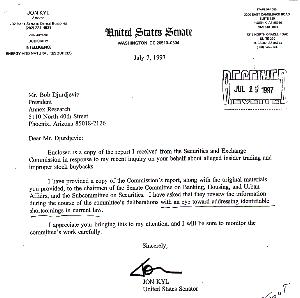

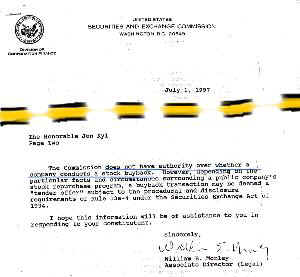

We’ve been writing about it ever since 1996, for example. We even exchanged correspondence back in July 1997 with vice president Al Gore, some U.S. senators, and the SEC. We thought it was a conflict of interest if officers sell their shares at the same time they are directing the company to buy back huge amounts of stock. That’s like selling deflated shares to yourself at market prices!

Vice President Gore thought we'd raised "an very interesting issue" that "merits thorough consideration." Senator Jon Kyl said he'd forwarded the information to the chairman of Senate's Banking, Housing and Urban Affairs and the Subcommittee on Securities, for "deliberations with an eye toward addressing identifiable shortcomings in current law." The SEC said it didn't have the jurisdiction over stock buybacks.

Yet our warnings have fallen on deaf ears. Which is proof positive that the unsavory actions that Gerstner, Lay, Skilling et. al. took are only symptoms of a larger problem. A macro view of these scandals shows that political plutocracy has replaced the once free and democratic America.

None of these scams or corporate abuses of power would have been possible had the government and/or the media done their job diligently and vigilantly.

“Silence is acquiescence,” goes an old saw. By remaining silent and passive, if not outright supportive of Gerstner, Lay, Skilling et. al., despite warnings about their self-dealings, the government and the media should bear their share of the responsibility.

If there is still justice in this land, the Justice Department should be prosecuting the heads of the SEC and the White House, and not just the Enron’s and the Andersen’s of the corporate world. And the people responsible for allowing plutocracy to usurp our traditional entrepreneurial American way of life, should be personally made to pay restitutions to the parties injured by Enron or IBM Greed, Inc. - specifically, the employees and shareholders of these companies.

That’s basically what William F. Buckley, Jr. also urged in his Jan. 25 National Review editorial, “Give It Back!”:

“The proposal here is that these seven

men simply return the money they made to the company - if possible,

directing its routing as a contribution to the 401(k) retirement funds

that evaporated in the meltdown. We are talking about $130 million. The

largest sums went to former CEO Jeffrey Skilling and to former chairman

Kenneth Lay.

It would be especially heartening if the

offerings were made before any consolidated investigation made likely

successful criminal prosecution. A gesture of the kind could detoxify

much of what happened. A $90 billion company can go down for reasons

that don't incriminate management. But when simultaneously, management

prospers, a transcendent moral question arises, and this has happened in

the case of capitalism vs. capitalists.”

Of course, Buckley was referring to Enron. But his case of “capitalism vs. capitalists” also applies to IBM and Sir Lou. In spades… as you saw in this report.

Happy bargain hunting!

Bob

Djurdjevic

Closing the Barn Door After the Horse Has

Gone?

Revelations

that executives at Global Crossing Ltd. and Enron Corp. were selling huge

stakes in their companies as the enterprises headed toward collapse have

spurred efforts in Washington to speed up disclosure of insider sales, the

Washington

Post reported on March 7.

Here’s an excerpt:

“The Securities and

Exchange Commission has proposed a regulation that would require insiders

to disclose their stock sales within just two days of closure. That would

be a dramatic change from current rules, under which some sales can occur

months before they are reported.

Rep. George Miller (D-Calif.) is pushing a

proposal that would require company executives to notify employees and

pension plans within 24 hours of a sale. Sen. Jean Carnahan (D-Mo.) has

proposed a bill that would require disclosure of insider sales on the same

day of a transaction.

Executives at Global Crossing sold more than $482 million worth of

shares as the industry declined in 2000 and 2001, but they had plenty of

company. Insider trading was particularly widespread throughout the

telecommunications industry as it went through the biggest boom in a

generation in 1998 and 1999 before going bust.”

Notice that, once again, IBM is not even mentioned even though Enron’s and Global Crossing’s insider sales are dwarfed by those by the Big Blue’s CEO and top officers?

[i] $115 million, according to IBM Proxy Statement 2001.

(an excerpt from the IBM 2001 Proxy Statement)

|

Compensation

for the Chairman and Chief Executive Officer As

he completes nine years as IBM's Chairman and Chief Executive

Officer, Mr. Gerstner has continued to demonstrate highly

effective leadership and vision in a volatile marketplace. Since

assuming his role in April of 1993, Mr. Gerstner has built upon

IBM's strengths and executed his strategic vision, positioning

IBM as a diversified leader at the center of the e-business

marketplace with a breadth of products and services unparalleled

in the industry. As a result, during his tenure through year-end

2001, stockholders have experienced a 938% increase in total

stockholder return. In a year which included a technology industry downturn

and the unprecedented events of September 11, IBM achieved stock

price growth of 42%, the second-highest performance among the 30

Dow Jones Industrial Average companies; achieved revenues of

$85.9 billion, 1% above last year's total at constant currency,

compared to a 2% decline in the technology industry; increased

market value by $60 billion; and achieved earnings-per-share of

$4.35, within 2% of last year's record earnings per share. These

results in an increasingly turbulent market reinforce the

strength of IBM's portfolio of businesses. Some highlights of

IBM's business performance (all at constant currency) include:

double-digit revenue growth in Global Services, driven by new

signings of $51 billion, resulting in a record backlog of $102

billion; double-digit revenue growth and market share gains in

IBM's Websphere, MQ Series and DB2 software; within eServer

platform, market share gains led by zSeries, and the successful

launch of the Regatta UNIX-based pSeries server in the fourth

quarter; and revenue growth of 11% year-to-year for Storage

Products. In addition, for the ninth consecutive year, IBM was

awarded more U.S. patents than any other company (3,411). The Committee's criteria for determining Mr. Gerstner's

compensation are driven by three factors: the competitive

marketplace, the complexity inherent in leading IBM (because of

its size, breadth of product and service offerings, global

reach, technology dependency, number of competitors and the

rate/speed of change in the IT industry) and,

most importantly, Mr. Gerstner's performance. The Committee believes that, in a year of volatility and

challenge in the marketplace, Mr. Gerstner's performance and leadership in

reaffirming IBM as the industry's premier e-business company and

in positioning IBM for continued growth was outstanding.

This is reflected in Mr. Gerstner's annual incentive award of

$8,000,000 for 2001, which is reported in the "Bonus"

column of the Summary

Compensation Table. He also earned a payout from the

1999-2001 long-term incentive program award based on the

Company's cumulative financial results over the three-year

period. The Committee further recognized Mr. Gerstner's efforts

to position IBM for the future by assisting in the transition of

his management responsibilities to the strong team of senior

leaders he has developed. On January 29, 2002, Mr. S. J.

Palmisano was elected by the Board of Directors as Chief

Executive Officer effective March 1, 2002, and Mr. Gerstner's

employment agreement was amended to reflect his agreement to

remain as Chairman until his retirement from the Company at age

61 in March 2003 or earlier with the Board's consent. Further,

the Committee recommended, and the Board approved, the grant to

Mr. Gerstner of a special restricted stock unit award covering

125,000 shares of IBM common stock, which will vest upon his

retirement from IBM. The Committee made this award in

consideration of Mr. Gerstner's willingness to extend his term

as Chairman, to recognize his outstanding performance and

leadership and to ensure that he continues to receive

competitive total pay for performance in line with other

top-performing business leaders, using data prepared by

independent consultants. The terms of Mr. Gerstner's employment

agreement are described in the section entitled, "Employment

Agreements and Change-in-Control Arrangements." |

{kind=link}

{kind=link}

{kind=link}